Source: Tencent Technology

On March 31, 2026, OpenAI announced the closure of its latest funding round at a post-money valuation of $852 billion, with total committed capital reaching $122 billion. This marks one of the largest financing events in Silicon Valley history. On the same day, OpenAI sold approximately $30 billion worth of shares to individual investors through banking channels for the first time and announced that its stock would be included in multiple ETFs managed by ARK Invest, led by Cathie Wood.

This company, which has yet to turn a profit and is projected to incur a loss of $14 billion in 2026, now boasts a valuation surpassing the vast majority of publicly listed companies globally. CFO Sarah Friar stated in an interview that the scale of this funding round 'far exceeds the largest IPO in history.'

A more noteworthy signal is the unprecedented enthusiasm of individual investors flooding into large-model companies. Whether it's closed-end funds in the United States such as $Fundrise Innovation Fund (VCX.US)$ 、 $Destiny Tech100 (DXYZ.US)$Should I go for closed-end funds, or those listed on the Hong Kong stock exchange?$KNOWLEDGE ATLAS (02513.HK)$and$MINIMAX-W (00100.HK)$, or companies listed on the Hong Kong Stock Exchange like and , individual investors worldwide are casting their votes with real capital for the future narrative of AGI (Artificial General Intelligence).

A more noteworthy signal is the unprecedented enthusiasm of individual investors flooding into large-model companies. Whether it's closed-end funds in the United States such as $Fundrise Innovation Fund (VCX.US)$ 、 $Destiny Tech100 (DXYZ.US)$Should I go for closed-end funds, or those listed on the Hong Kong stock exchange?$KNOWLEDGE ATLAS (02513.HK)$and$MINIMAX-W (00100.HK)$, or companies listed on the Hong Kong Stock Exchange like and , individual investors worldwide are casting their votes with real capital for the future narrative of AGI (Artificial General Intelligence).

01 Valuation Logic: Surging Revenue, Distant Profitability

How should we interpret the valuations of large-model companies?

OpenAI’s revenue was approximately $2 billion in 2023, $6 billion in 2024, and $13.1 billion in 2025. According to publicly available data, as of the end of February 2026, OpenAI's annualized revenue had surpassed $25 billion, representing growth of over four times within 14 months. OpenAI claims its API processes more than 15 billion tokens per minute, with enterprise revenue accounting for over 40%.

Anthropic's growth curve is steeper. Annualized revenue is expected to surge from several billion dollars in 2025 to nearly 10 billion dollars, with market expectations for its 2026 revenue continuing to rise. In February 2026, Anthropic completed a Series G funding round of 30 billion dollars at a valuation of 380 billion dollars.

However, on the flip side of this rapid revenue growth are equally staggering losses. OpenAI is projected to incur a loss of approximately 14 billion dollars in 2026, with annual cash burn expected to reach 57 billion dollars by 2027. According to data from Sacra, OpenAI's gross margin is only about 33%, with inference costs reaching 8.4 billion dollars in 2025 and projected to rise to 14.1 billion dollars in 2026. Based on internal forecasts, OpenAI is not expected to achieve positive cash flow until at least 2030.

Dividing a valuation of 852 billion dollars by an annualized revenue of 25 billion dollars, OpenAI's current price-to-sales ratio is approximately 34 times. Dividing a valuation of 380 billion dollars by an annualized revenue of 19 billion dollars, Anthropic's price-to-sales ratio is approximately 20 times. For comparison, Microsoft's current price-to-sales ratio is about 12 times, while Google's is approximately 6 times.

In a sense, the price-to-sales ratio measures how much premium the market is willing to pay for each dollar of revenue generated by the company. Amazon's price-to-earnings ratio often exceeded 300 times or was even negative in the early 2010s, but its price-to-sales ratio was roughly between 1 and 2 times, which in hindsight was not unreasonable as AWS eventually delivered significant profits.

If measured by the price-to-earnings ratio, OpenAI currently has no profitability, and internal projections disclosed by multiple foreign media outlets indicate that it will not become profitable for several years. This is precisely the 'Price-to-Dream Ratio': investors are buying into the belief that AI will transform everything.

02. Samples of Chinese Large Model Listings

While the valuations of OpenAI and Anthropic remain 'paper wealth' within the private market, two large model companies in China have already faced public market pricing tests on secondary exchanges, with similarly optimistic results.

On January 8, 2026, Zhipu went public on the Hong Kong Stock Exchange as the 'world's first large model stock,' with an issue price of 116.2 Hong Kong dollars, corresponding to a market capitalization of approximately 52 billion Hong Kong dollars. The Hong Kong public offering was oversubscribed by 1,159 times. As of April 1, Zhipu's share price surged to 938 Hong Kong dollars, giving it a market capitalization exceeding 400 billion Hong Kong dollars, surpassing Baidu, JD.com, and Kuaishou.

MiniMax, which went public shortly after, saw its share price double on its debut day and continued to climb thereafter. On March 18, 2026, following the release of its next-generation M2.7 model, MiniMax's share price surged over 28%, with its market capitalization exceeding 380 billion Hong Kong dollars.

Zhipu reported total revenue of 724 million RMB for 2025, with a net loss of 4.718 billion RMB. MiniMax's revenue for 2025 was approximately 79.04 million US dollars (approximately 550 million RMB), with an adjusted net loss of around 250 million US dollars (approximately 1.75 billion RMB).

According to Choice data, as of March 2026, the price-to-sales ratios of Zhimap and MiniMax have reached hundreds of times. Meanwhile, Tencent's price-to-sales ratio is approximately 7 times, while Alibaba's is around 2.4 times.

However, sharp rises and falls are always intertwined. The monthly volatility of Zhimap and MiniMax reached as high as 109% and 81%, respectively. On March 10, the combined market value of the two companies soared by over HKD 100 billion in a single day, only to lose more than HKD 42 billion collectively the following day.

Section 03: Entry Channels for Individual Investors—from VCX to ARK, a Liquidity Relay

For global retail investors, directly purchasing shares of OpenAI or Anthropic is virtually impossible. Secondary market platforms like Forge Global and EquityZen require accredited investor status, with minimum thresholds typically ranging from USD 25,000 to USD 100,000, and waiting lists lasting up to six months.

Scarcity generates FOMO (Fear of Missing Out).

However, in the first quarter of 2026, multiple new channels were opened:

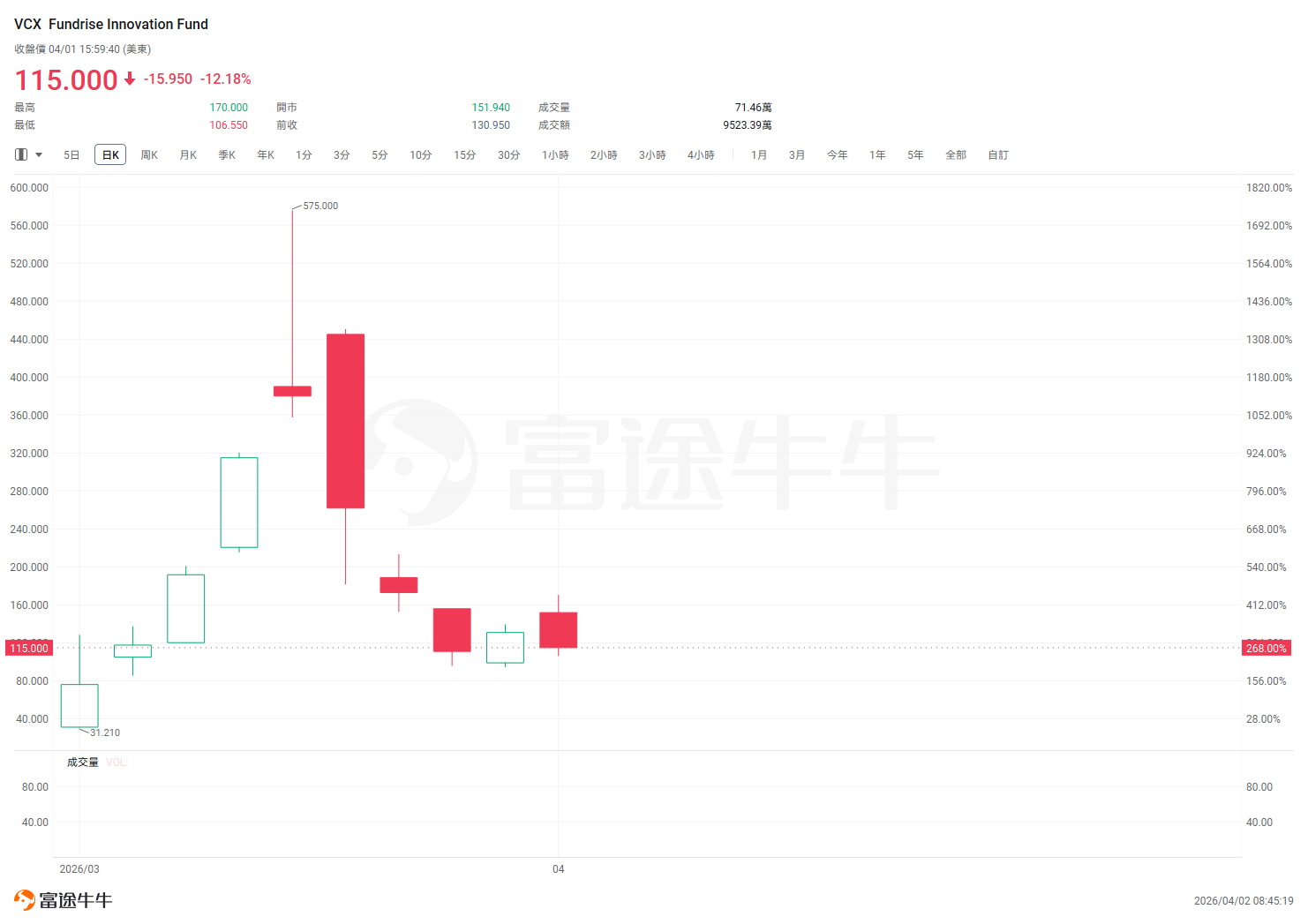

The first channel is closed-end funds. Fundrise Innovation Fund (VCX) was listed on the New York Stock Exchange on March 19, 2026, with a net asset value of approximately USD 18.97 per share. This fund holds stakes in private companies such as Anthropic (20.7%), Databricks (17.7%), OpenAI, and SpaceX.

On its debut trading day, VCX opened at around USD 42 and surged from dozens of dollars to nearly USD 575 within days after listing, reflecting a premium of more than 31 times.

Another closed-end fund, Destiny Tech100 (DXYZ), holds approximately 16.2% of SpaceX and gained indirect exposure to Anthropic through a $100 million SPV investment in January 2026. As of the end of 2025, DXYZ's net asset value per share was about $19.97, representing a 76% increase from the previous quarter and over 210% year-over-year growth.

The second channel is thematic ETFs. The AGIX ETF under KraneShares directly holds shares in Anthropic and xAI, while also allocating investments in tech giants such as Microsoft, Alphabet, Amazon, and NVIDIA, which indirectly own stakes in AI companies. Since its inception, the fund has significantly outperformed the S&P 500 and Nasdaq.

The third channel has just opened. On March 31, OpenAI announced that its shares would be included in three ETFs managed by ARK Invest—its flagship product ARKK (ARK Innovation ETF), ARKF (Blockchain & Fintech ETF), and ARKW (Next Generation Internet ETF). ARK previously held stakes in private companies like OpenAI and SpaceX through its venture capital fund, ARK Venture Fund (ARKVX). ARKVX is open to all investors with a management fee of only 2.75%, without charging the traditional 20% performance fee typical of venture capital funds.

However, amidst the frenzy, short-selling institutions have already begun to act. On March 26, Citron Research announced it was shorting VCX, citing a severe disconnect between its market price and net asset value. It referenced Fundrise’s 2023 case, where the company was fined $250,000 by the SEC for failing to disclose payments to over 200 influencers for promotional activities. VCX plummeted nearly 50% on the same day, closing at $262. Citron projected that if the premium were to revert to levels comparable to DXYZ, VCX could drop to $26, close to its net asset value.

Seeking Alpha also issued a 'Strong Sell' rating, pointing out that the implied valuations of VCX's top three holdings had exceeded the combined market capitalizations of NVIDIA, Apple, Google, Microsoft, Amazon, and Taiwan Semiconductor. The lock-up period expiring in September 2026 is seen as a critical inflection point, when 100,000 pre-listing investors will gain the freedom to sell, potentially causing a sudden surge in supply that could rapidly compress the premium.

A primary market investor commented, 'VCX surged from a net asset value of $19 to a peak of $575 in its first week of listing. This speed and magnitude are not indicative of allocation behavior but rather represent classic event-driven speculation.'

Is there a smooth exit path for retail investors? VCX and DXYZ trade on the NYSE, seemingly allowing sales at any time, but there is a structural trap: the fund shares are traded frequently on public markets, while the underlying assets consist of highly illiquid shares in private companies.

Once sentiment reverses and everyone simultaneously tries to sell an asset that cannot be liquidated at the base level, prices can quickly collapse toward or even below net asset value. DXYZ has already experienced one such cycle.

04. How much longer will the window of opportunity remain open?

All excitement ultimately points to the same milestone: the IPO.

According to multiple media reports, OpenAI is targeting a potential listing in the fourth quarter of 2026 or the first quarter of 2027. Anthropic has also engaged Wilson Sonsini as its IPO legal advisor and held preliminary discussions with investment banks.

Among China’s large model companies, Zhipu and MiniMax have already gone public, but greater anticipation lies in whether more large model companies will follow suit. The latest round of funding for MoonShot (Kimi) has valued the company at $18 billion. According to media reports, StepFun is also actively preparing for an IPO.

However, the IPO window does not remain open indefinitely. Newly listed companies are facing an imminent stress test: the wave of lock-up expirations. Both Zhipu and MiniMax went public in early January 2026. Following the Hong Kong stock market convention, the 6-to-12-month lock-up periods for cornerstone investors and internal shareholders will expire progressively from the second half of 2026 to early 2027.

Zhipu’s 11 cornerstone investors subscribed to HKD 2.98 billion, while MiniMax similarly brought in numerous strategic shareholders and employee shareholding platforms. Once the lock-up period ends, selling pressure will directly impact the floating shares.

On the U.S. stock side, the 100,000 pre-IPO investors of VCX are expected to see their lock-up periods expire in September 2026. Seeking Alpha predicts that the sudden increase in supply may quickly push its premium toward book value from current levels.

The macro environment is also narrowing the window. In the first quarter of 2026, the Magnificent Seven ETF (MAGS) fell by 16%, marking its worst quarterly performance since its inception in 2023. The U.S.-Iran conflict has driven up oil prices, exacerbating global uncertainty. If technology stocks continue to face pressure and the return on AI investments comes under greater scrutiny, the dual pressures of IPOs and lock-up expirations may arrive simultaneously.

Historically, the post-IPO performance of high-growth, high-loss tech companies has been highly dependent on market sentiment. During the 2021 wave of listings, many SaaS companies experienced continuous declines in their stock prices after going public at high valuations.

Valuations will eventually be tested by the market and revert to objective levels over the long term.

Until then, the liquidity provided by retail investors, the divergence among institutional investors, and geopolitical uncertainties will continue to intertwine, shaping one of the most expensive technological narratives of our time.

05, Perspectives from Institutional Investors

Notably, institutional investors exhibit a far more cautious attitude compared to retail investors.

Aswath Damodaran, Professor of Finance at New York University's Stern School of Business, publicly stated that after stripping out the computational power commitments and conditional investment tranches, the actual cash infusion in OpenAI's $122 billion financing is significantly smaller than the headline figure. He pointed out that the revenue growth rate implied by the $852 billion valuation is 'something no technology company of comparable scale has ever consistently achieved.'

Wall Street’s skepticism about the financing structure is growing. Of Amazon’s $50 billion investment, $35 billion is contingent upon OpenAI’s IPO or achieving AGI; NVIDIA’s $30 billion contribution is primarily in computational capacity rather than cash; and SoftBank’s $30 billion is disbursed in three tranches. Some analysts have described this model as 'internal circulation financing,' where companies mutually invest and procure services from one another, artificially inflating each other’s revenues and valuations.

PitchBook’s research findings are even more direct: among the three major AI IPO candidates—OpenAI, Anthropic, and Databricks—OpenAI scores the lowest on fundamental business metrics despite having the highest valuation. Morningstar noted that OpenAI has never publicly disclosed its enterprise customer retention rate, which represents a significant information gap for a company on the verge of going public with a trillion-dollar valuation.

However, institutions are not entirely bearish. JPMorgan has assigned Zhipu a 'buy' rating, while Goldman Sachs previously analyzed that the global competitiveness of Chinese AI models would bring in over $200 billion in capital inflows.

The crux of the divergence lies mainly in the time horizon. In the short term, large model companies’ valuations are almost entirely predicated on growth expectations and narrative premiums; in the long term, if OpenAI truly achieves its projected $280 billion in revenue and 15% operating profit margin by 2030, an annual profit of $42 billion would be sufficient to justify a trillion-dollar market capitalization.

The challenge, however, is that there are too many variables along the path to that future.

Editor /rice