The Hong Kong stock market's new listings sector got off to a roaring start in the first quarter of 2026.

In just three short months, a flood of new stocks has surged into the market,$HKEX (00388.HK)$including AI-driven large model enterprises with their own halos, domestic GPU leaders, and star surgical robotics companies… Not only have they injected fresh vitality into the market, but they have also sparked an impressive wave of stock price enthusiasm in the secondary market. Meanwhile, dual listings on 'A+H' exchanges have emerged as a unique trend, adding significant depth to Hong Kong’s equity landscape.

For a time, capital, attention, and expectations all converged here.

Raising over HKD 100 billion to claim the global top spot, 'A+H' dominates the top ten listings.

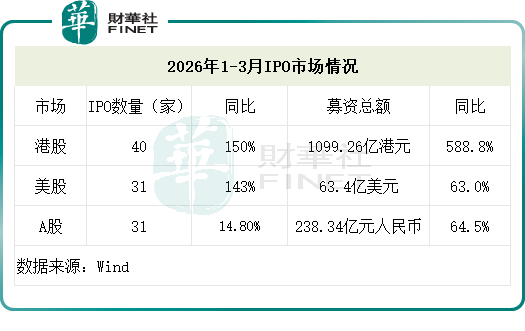

First, let's look at some hard-core data: According to Wind data, in the first quarter, a total of 40 companies went public on the Hong Kong Exchange, raising a cumulative net amount exceeding HKD 100 billion, reaching HKD 109.926 billion, a year-on-year surge of 588.8%. This not only set a record for the fastest-ever breakthrough of the HKD 100 billion mark but also propelled Hong Kong to the top spot in global IPO fundraising.

First, let's look at some hard-core data: According to Wind data, in the first quarter, a total of 40 companies went public on the Hong Kong Exchange, raising a cumulative net amount exceeding HKD 100 billion, reaching HKD 109.926 billion, a year-on-year surge of 588.8%. This not only set a record for the fastest-ever breakthrough of the HKD 100 billion mark but also propelled Hong Kong to the top spot in global IPO fundraising.

Notably, this quarter did not see any mega-IPOs like those in 2025, except for$MUYUAN (02714.HK)$and$EASTROC (09980.HK)$, whose financing barely exceeded HKD 10 billion. Even so, the total funds raised still far surpassed last year’s same period, demonstrating a notable acceleration in market issuance pace.

Comparing horizontally further highlights the achievement: during the same period, the US market saw 31 new IPOs, an increase of 143% year-on-year, raising a combined net amount of approximately USD 6.34 billion (about HKD 49.7 billion), up 63% year-on-year. The A-share market had 31 new IPOs, growing by 14.8% year-on-year, with a total net amount of approximately RMB 27.1 billion, increasing by 64.5% year-on-year. Whether measured by scale or growth rate, Hong Kong equities are leading the pack.

In this round of Hong Kong IPO fervor, 'A+H' shares undoubtedly shone brightest – both in quantity and size.

In the first quarter, a total of 16 A-share companies successfully listed on the Hong Kong Exchange, achieving dual listings. In terms of fundraising amounts, A+H shares strongly occupied seven out of the top ten IPO slots, among which$MUYUAN (02714.HK)$、$EASTROC (09980.HK)$raised over HKD 10 billion each,$MONTAGE TECH (06809.HK)$and$HANS CNC (03200.HK)$also raised net proceeds exceeding HKD 5 billion. In aggregate, A+H shares raised a net amount of HKD 68.2 billion in the first quarter, accounting for a high 62% and firmly securing the top position in market fundraising.

This robust trend is no accident. Continuous inflows of capital from both domestic and overseas markets into Hong Kong stocks have provided ample liquidity support for new share issuance; the Hong Kong Exchange has been continuously advancing its listing system reforms, particularly with the implementation of Chapter 18C (Specialized Technology Company Listing Regime), creating a convenient channel for hard-tech enterprises in fields such as artificial intelligence, semiconductors, and robotics; coupled with the concentrated release of pent-up IPO demand during this quarter, the return of large-scale projects like Muyuan Foods and Dongpeng Beverages has also directly driven up overall fundraising levels.

Moreover, the proportion of fundraising by mature enterprises has notably increased. According to Wind data, over 80% of contributions came from mature enterprises that already possessed stable profitability or industry-leading positions prior to listing, while less than 5% of fundraising was accounted for by three unprofitable enterprises.

Investors cast their votes with real money: the first-day break-even rate was only 12.5%.

Is the market buying in? The enthusiasm of investors provides the most direct answer.

The subscription performance of Hong Kong's IPO market in the first quarter demonstrated a highly polarized pattern. According to Wind data, new economy enterprises generally received extremely high subscription multiples. Among them,$HUAYAN ROBOTICS (01021.HK)$achieved a public offering subscription multiple as high as 5059.38 times,$EXTREME VISION (06636.HK)$also reached a placement subscription multiple of 4591.37 times, far exceeding the market average. In contrast, some traditional industry enterprises appeared less popular, such as in the semiconductor sector,$OMNIVISION (00501.HK)$and$MUYUAN (02714.HK)$, with subscription multiples of only 9.28 times and 5.88 times, respectively.

This striking disparity vividly reveals the current core preference of capital: scarce hard-tech targets are truly the 'darlings' of the market.

In terms of debut-day performance, newly listed stocks from Hong Kong's IPOs in the first quarter delivered impressive results, reflecting heightened investor enthusiasm. Among the 40 newly listed stocks,$HAIZHI TECH GP (02706.HK)$The stock with the largest increase surged by 242.2% on its first day, while others such as$EXTREME VISION (06636.HK)$、$DIAGENS-B (02526.HK)$and$MINIMAX-W (00100.HK)$and five other stocks all doubled in value; regarding initial public offerings breaking below issue price, only five stocks fell below their issue price on the first day of listing, with a break-even rate as low as 12.5%. By comparison, research statistics from CITIC Securities show that the break-even rate for new Hong Kong stocks in 2025 was as high as 27.6%.

What are the reasons behind this significant improvement in the break-even rate? There are three key factors: First, the quality of listed companies has significantly improved. Enterprises specializing in AI and robotics possess technological scarcity and growth certainty, attracting substantial capital inflows; second, the financial environment has markedly warmed up. Global capital is accelerating its return to Chinese assets, and long-term funds such as insurance capital have actively entered the market as cornerstone investors, providing stable 'ballast' for several IPOs in the first quarter; third, the market ecosystem continues to optimize.

New economies like AI and robotics are creating a whirlwind

Through the above data, a deeper trend is emerging: the internal structure of Hong Kong's IPO market is undergoing a profound and clear transformation.

The new economy sector, especially hard technology fields represented by semiconductors, artificial intelligence, and robotics, has leapt from being an 'important participant' in the past to becoming the 'dominant force' in the market. The leader in AI large models,$KNOWLEDGE ATLAS (02513.HK)$, and the leader in domestic GPUs$BIREN TECH (06082.HK)$, the leading surgical robotics company$EDGE MEDICAL-B (02675.HK)$… These 'hard tech stars' saw overwhelming subscription demand during their IPO periods, with equally impressive stock price performances.

This dominance is first reflected in the scale of financing. According to Wind data, new economy enterprises (primarily in the semiconductor, AI, and robotics sectors) collectively raised HKD 45.657 billion in Q1, accounting for 41.6% of the market's total financing. This indicates that nearly half of all market financing activities were driven by new economy enterprises, underscoring their importance far beyond traditional industries. This highly concentrated financing structure clearly demonstrates that, amid global industrial chain restructuring and accelerated domestic substitution, the capital markets are providing top-tier funding support and valuation recognition to hard technology sectors.

A longitudinal comparison further highlights this trend: The proportion of new economy enterprises in Hong Kong's IPO market has significantly increased from 7.04% for the whole of 2023 to 30.0% in Q1 2026. Meanwhile, their share of total financing has risen from 37.96% in Q4 2025 to 41.6%, showing a steady upward trajectory.

In recent years, through systematically lowering the listing barriers for hard tech companies, the Hong Kong Exchange has sent a clear signal to the market: actively embracing the new economy and supporting the national innovation-driven development strategy. This strategic positioning has attracted a large number of eligible companies to submit applications, forming a robust pipeline. As of March 31, 2026, among the 368 companies queued for listing on the Hong Kong Exchange, as many as 241 belong to the new economy sector, representing approximately 65.5%. This suggests that hard tech will continue to dominate Hong Kong's IPO landscape for some time to come. In particular, there are abundant reserves in sectors such as semiconductor products, electronic components, information technology services, and biotechnology as well as innovative pharmaceuticals.

Conclusion: After the surge, where is the market heading?

The Hong Kong IPO market in Q1 delivered three strong responses—billions in fundraising, low post-IPO price drops, and hard tech dominance—demonstrating its robust resilience and vitality.

Beneath the surface of overall prosperity, the market structure is undergoing profound transformation: capital is highly concentrated towards leading enterprises and new economy hard tech sectors, while investor sentiment is becoming more rational amid optimism. The strong comeback of A+H shares, the benefits released by Chapter 18C, and the inflow of global capital have together shaped the multiple dimensions of this quarter’s IPO boom.

The bustling Q1 has passed, leaving key questions ahead: Can this momentum be sustained? Will the new economy-led landscape strengthen further? For investors, while embracing the opportunities in hard tech, it is also crucial to be wary of individual stock differentiation risks. However, at the very least, the start of 2026 has already written an encouraging prelude for the Hong Kong market.

Editor/Melody