The head of Standard Chartered's commodities research noted that gold often becomes a passive liquidation tool in the early stages of a crisis, with historical suppression periods typically lasting 4 to 6 weeks. Although the current downturn has been more severe, overheated positions have largely been cleared, and gold is expected to regain upward momentum in the coming months, challenging historical highs.

The safe-haven status of gold has once again come under scrutiny. Since the outbreak of the conflict in the Middle East, $XAU/USD (XAUUSD.CFD)$ gold prices have plummeted significantly. This contradicts the conventional view that gold, as a safe-haven asset, provides stability (or even appreciation) during periods of market turbulence, heightened uncertainty, or geopolitical tensions. However, Suki Cooper, Global Head of Commodities Research at Standard Chartered Bank, argues that despite gold’s temporary role shift in the short term, its status as a safe-haven asset remains intact, and she expects gold prices to challenge historical highs once again. Her perspective is as follows.

Gold can act as both a leading player and a supporting role in the market, but this does not imply it has lost its traditional functions.

During times of crisis, investors rotate between assets, and stock market losses may also trigger margin calls. Gold is one of the few assets that can be readily liquidated to provide liquidity without significant risk of substantial losses.

During times of crisis, investors rotate between assets, and stock market losses may also trigger margin calls. Gold is one of the few assets that can be readily liquidated to provide liquidity without significant risk of substantial losses.

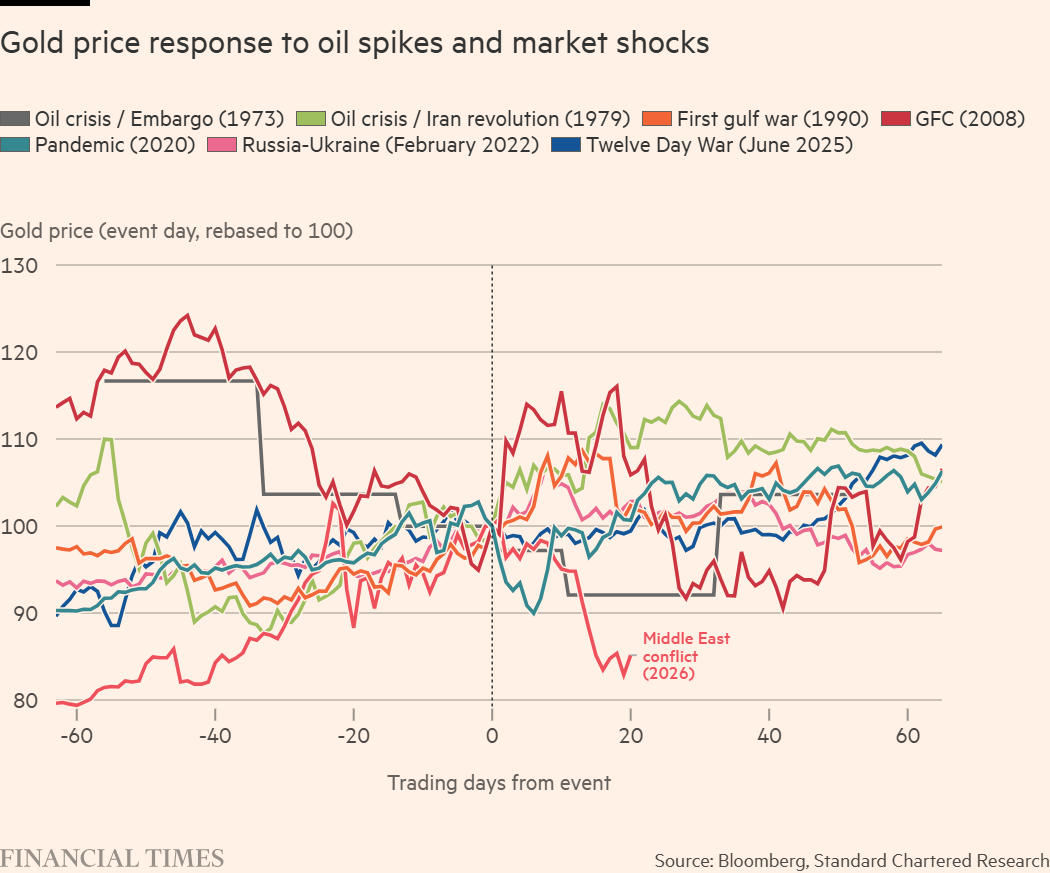

Historically, such liquidity needs tend to weigh on gold prices for about four to six weeks following the onset of a crisis; once liquidity pressures ease, investors typically resume accumulating gold. If the crisis persists, this process may take longer — for instance, during the global financial crisis, it took gold more than four months to recover its losses.

Although the recent decline in gold prices far exceeds those observed during previous geopolitical conflicts (especially wars in the Middle East), this divergence is not without cause.

In January, gold prices hit record highs, and exchange-traded products (ETPs) tracking gold prices surged to new levels amid skyrocketing investor demand, making gold a prime target for selling. The premium of spot gold prices over the 50-day moving average soared to its highest level since 1999. Now, the situation has reversed: spot gold prices have fallen below the 50-day moving average, with the deviation reaching its widest point since 2013. Gold, which was in an overbought condition in January, shifted to an oversold state after the outbreak of the conflict.

Gold Price Response to Oil Price Surges and Market Shocks

So, what signal is the movement in gold prices sending? First, there remains uncertainty in the market regarding the duration of the conflict, with liquidity needs persisting. The spike in gold's implied volatility to levels seen during the pandemic period serves as evidence.

Gold is now reverting to a state where its short-term performance is once again dominated by expectations of U.S. interest rates and uncertainties surrounding policy responses to the current crisis.

In the long term, if market expectations for interest rate hikes strengthen, the opportunity cost of holding gold rises (since gold does not generate dividends or interest), and gold prices tend to fall. This correlation temporarily broke down at the end of 2022 due to central bank gold purchases, but in recent weeks, as expectations for U.S. interest rate cuts this year have cooled, the relationship has resumed.

ETP fund flows and central bank gold purchases are two key indicators to watch. ETP investors focus more on real yield expectations rather than structural drivers. In March, net redemptions from ETPs may reach their highest level since September 2022, indicating that short-term funds are moving away from gold's structural and safe-haven allocation logic. However, the pace of ETP selling has begun to slow, suggesting that previously overheated positions may have largely been cleared.

On the central bank front, the market is watching for signs of potential sales from their accumulated gold reserves in recent years. Last year, central banks' net gold purchases slowed from over 1,000 tons to 863 tons, but in dollar terms, they still hit a record high.

At the same time, there are ample reasons supporting higher gold prices. The current price does not reflect the risk of an economic recession. During recessions, gold typically averages gains of 15%, while industrial commodities are weighed down by declining output.

Additionally, gold prices do not yet reflect concerns about stagflation. Even if conflicts were to end tomorrow, oil prices are likely to remain elevated for longer, exacerbating inflationary pressures. As a store of value, gold tends to strengthen in an environment of rising inflation, especially when inflation exceeds expectations and persists.

Many of gold's structural drivers remain intact, including concerns about high debt levels in the U.S. and globally, currency devaluation, tariff and trade uncertainties, and geopolitical risks.

Gold currently reflects multiple risks simultaneously, making its short-term trajectory non-linear. Existing liquidity pressures may continue to weigh on gold prices for some time. However, we still expect gold prices to rebound in the coming months. On the downside, gold's 200-day moving average, which has held firm since October 2023, provides strong support. The broader trend for the gold market remains upward.

This article is from Suki Cooper, Global Head of Commodities Research at Standard Chartered Bank.

Editor/Doris