In the first quarter of 2026, global capital markets fluctuated repeatedly amid geopolitical and economic uncertainties. As a key market connecting mainland and global funds, Hong Kong's stock market exhibited a highly contradictory performance this quarter, which is worth analyzing: on one hand, trading remained vibrant, with daily average turnover maintaining at historically high levels; on the other hand, there was a significant shift in capital flows and risk appetite. The pace of Southbound funds' “shopping spree” abruptly slowed, the luster of technology stocks dimmed, while the new share market continued the prosperity seen in the second half of 2025.

Active trading masks index weakness as risk aversion drives HALO trades.

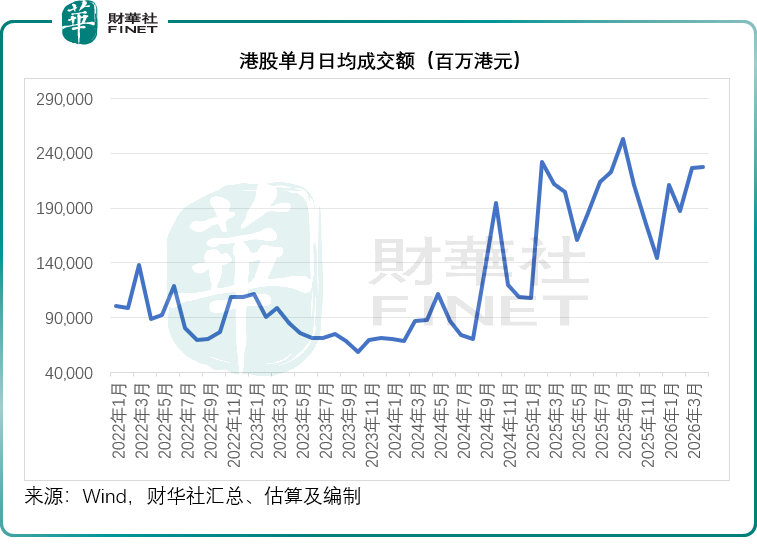

In the first quarter of 2026, Hong Kong’s stock market presented a deceptive kind of “prosperity.” From a liquidity perspective, market activity remained at a high level, with daily average turnover consistently above the HKD 200 billion mark: January recorded an average daily turnover of HKD 210.89 billion, February (which included the Lunar New Year) saw HKD 187.33 billion, and March further rose to HKD 226.219 billion, as shown in the chart below, indicating sustained trading enthusiasm. However, this high liquidity did not translate into broad-based index gains but instead reflected defensive sentiment amidst uncertainty.

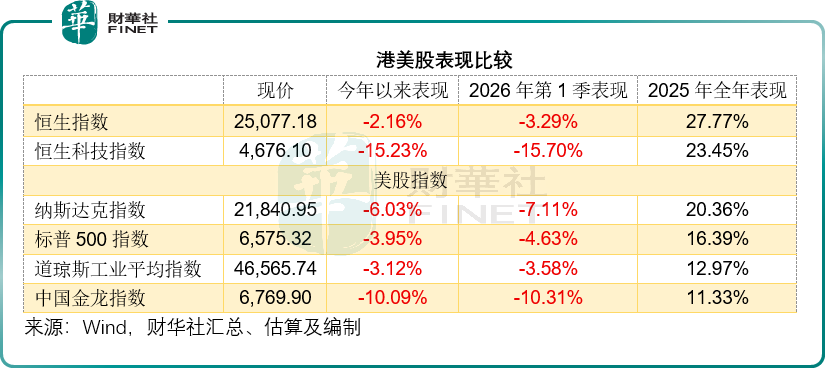

The broader market demonstrated pronounced defensive characteristics. $Hang Seng Index (800000.HK)$ As the stronghold of blue-chip stocks, the Hang Seng Index fell by 3.29% in the first quarter. Although it posted negative returns, its performance was notably better than that of the technology growth sector and slightly outperformed major U.S. blue-chip indices, $Dow Jones Industrial Average (.DJI.US)$ which declined by approximately -3.58%. In comparison, $Hang Seng TECH Index (800700.HK)$ the tech-heavy index plummeted by 15.70%, significantly underperforming both the Hang Seng Index and major U.S. technology stock indices. $Nasdaq Composite Index (.IXIC.US)$ -7.11%。

This divergence may be primarily attributed to the current market’s dominant logic shifting toward HALO (Heavy assets, low obsolescence) trading strategies—favoring companies less affected by AI, such as those in heavy assets, logistics, and energy sectors, while shunning overvalued AI and tech stocks. Against the backdrop of rising geopolitical risks (e.g., tensions in the Middle East), oscillating expectations of Fed rate cuts, Trump’s rhetoric influencing capital flows, and tariff concerns, funds rapidly withdrew from high-valuation, high-volatility tech growth stocks and flowed into low-valuation, high-dividend defensive blue-chips.

This divergence may be primarily attributed to the current market’s dominant logic shifting toward HALO (Heavy assets, low obsolescence) trading strategies—favoring companies less affected by AI, such as those in heavy assets, logistics, and energy sectors, while shunning overvalued AI and tech stocks. Against the backdrop of rising geopolitical risks (e.g., tensions in the Middle East), oscillating expectations of Fed rate cuts, Trump’s rhetoric influencing capital flows, and tariff concerns, funds rapidly withdrew from high-valuation, high-volatility tech growth stocks and flowed into low-valuation, high-dividend defensive blue-chips.

Southbound funds ‘shift from offense to defense,’ recording net outflows in April.

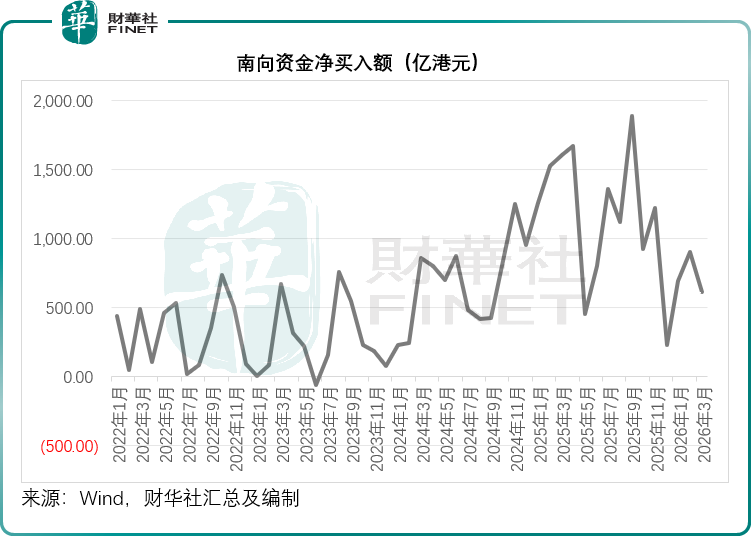

As a crucial determinant of pricing power in Hong Kong’s stock market over the past two years, the behavior pattern of Southbound funds underwent subtle changes in the first quarter of 2026. Wind data shows a marked contraction in Southbound funds’ net buying scale. Monthly net inflows for the first three months of 2026 were all below HKD 100 billion, compared to over HKD 150 billion per month in the same period last year. On April 1st, Southbound funds even recorded a net outflow of HKD 12.694 billion, occurring against the backdrop of a global stock market rally, potentially signaling mainland funds taking profits or adjusting positions during the rebound window, suggesting short-term caution about equity market prospects.

Primary Market: IPO Financing Scale Surpasses Secondary Financing

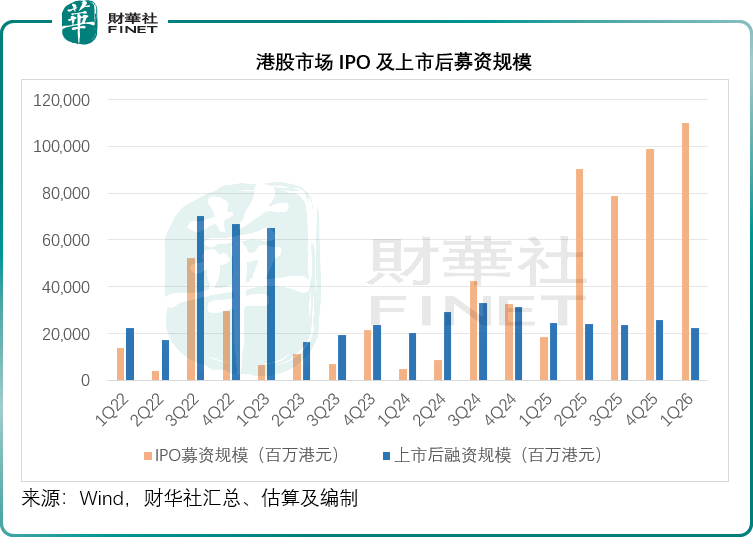

In sharp contrast to the cautious secondary market, the Hong Kong stock IPO market experienced a 'highlight moment' in Q1 2026, with total initial fundraising exceeding HKD 109.9 billion, surging nearly fivefold year-on-year.

A review of historical data shows that over the past few years, the scale of secondary financing (post-listing financing) in the Hong Kong stock market has generally been higher than or equal to the scale of new share offerings. However, the robust new share market since Q2 2025 reversed this trend, as shown in the chart below.

This wave of IPO enthusiasm exhibits strong structural characteristics:

Continued A+H share listing trend: $MUYUAN (02714.HK)$ 、 $EASTROC (09980.HK)$ Industry leaders going public in Hong Kong, with individual fundraising exceeding RMB 10 billion, demonstrate the recognition of high-quality mainland assets for the Hong Kong platform.

Hard tech comeback: Benefiting from the optimization of Chapter 18C, $KNOWLEDGE ATLAS (02513.HK)$ 、 $MINIMAX-W (00100.HK)$ AI unicorns and $HUAYAN ROBOTICS (01021.HK)$ 、 $GALAXIS TECH (02729.HK)$ $BIREN TECH (06082.HK)$ hard tech companies successfully listed, showing strong post-IPO performance, with some even doubling.

However, behind the prosperity lie concerns, presenting a 'polarization.' On one hand, chip stocks and large model stocks favored by the market have performed impressively; on the other hand, some traditional consumer goods and healthcare new shares lacking compelling narratives faced insufficient subscriptions or even failed issuance (e.g., Tongrentang Healthcare delaying its IPO).

The 'bloodletting' effect of global IPOs is approaching: The tidal waves of SpaceX and OpenAI

It is worth noting that this year, the global primary market will witness the listing of mega-cap companies, which may fundamentally alter the distribution of capital.

SpaceX has recently filed its IPO application confidentially. Market expectations suggest its valuation at listing could reach as high as $1.75 trillion, with a potential financing scale of $50 billion, or approximately HKD 400 billion—higher than the total IPO financing volume in the Hong Kong stock market for the 12 months ending March 2026.

Additionally, OpenAI has just completed a new round of financing, raising $122 billion, close to HKD 1 trillion, and is highly likely to complete its IPO within 2026, with a significant financing scale expected.

The sheer size of these 'mega-cap' companies is sufficient to trigger tidal shifts in global speculative capital flows: global sovereign wealth funds, long-term mutual funds, hedge funds, and even retail investors will concentrate their attention and positions on these 'symbols of the era.' Emerging markets (including Hong Kong stocks) may face phased net capital outflows; the pricing of trillion-dollar AI companies after their IPOs will redefine the valuation framework for global technology stocks, potentially suppressing the growth prospects of AI concept stocks listed in Hong Kong, such as Zhipu and MiniMax.

For Hong Kong stocks, the risk lies in the possibility that when global speculative capital is drawn to these 'aircraft carrier'-level IPOs, the liquidity premium of Hong Kong stocks themselves may be compressed, particularly affecting newly listed stocks and tech stocks that lack scarcity and whose valuations have already been priced in advance, subjecting them to more severe tests.

Summary: Heightened volatility makes stringent valuation scrutiny inevitable

Looking ahead to subsequent trends in 2026, the Hong Kong stock market will face dual pressures: first, the diversion of global capital caused by mega-cap IPOs worldwide, with companies like SpaceX and OpenAI continuing to attract global speculative capital, impacting the capital availability in Hong Kong stocks; second, internal capital diversion due to persistently robust IPO activity in Hong Kong itself, alongside growing market scrutiny over the valuations of both IPOs and secondary-market stocks.

Going forward, both the existing stocks in the Hong Kong secondary market and upcoming IPOs will undergo stricter valuation assessments. Assets lacking core competitiveness and carrying excessive valuations may face risks of valuation corrections; whereas low-valuation, high-dividend defensive blue-chip stocks, as well as hard-tech enterprises with core technological advantages, may deliver relatively stable performances amid volatility. For investors, it is essential to clearly understand the current volatility dynamics of Hong Kong stocks, avoid blindly following trends, closely monitor changes in external variables, and focus on quality assets to navigate risks and seize opportunities in a complex market environment.

Editor/Jayden