①Goldman Sachs stated that with the early approval of Eli Lilly and Co's oral weight-loss drug, the company is entering a new cycle of key product launches; ②The FDA’s labeling for Foundayo aligns with the existing framework for GLP-1 drugs, with no new risks identified in terms of safety or usage restrictions; ③Goldman Sachs maintains a “Buy” rating for Eli Lilly and Co, with a 12-month target price of $1,260.

Cailian Press reported on April 2 (edited by Xia Junxiong) that Goldman Sachs stated in its latest research report that, with the early approval of $Eli Lilly and Co (LLY.US)$ oral weight-loss drugs, the company is set to enter a new cycle of key product launches. Goldman Sachs maintained its 'Buy' rating for Eli Lilly and Co and assigned it a target price of $1,260.

A Goldman Sachs analyst team led by Asad Haider released a report on April 1 detailing the impact of the approval of Eli Lilly and Co’s oral GLP-1 weight-loss drug Orforglipron (now named Foundayo) and the company’s financial outlook.

On April 1 local time, the U.S. Food and Drug Administration (FDA) approved Foundayo for market release, earlier than the market-expected date of April 10 (PDUFA date). This early approval aligns with Eli Lilly and Co management’s projection that Foundayo would be approved in “early Q2 2026.”

On April 1 local time, the U.S. Food and Drug Administration (FDA) approved Foundayo for market release, earlier than the market-expected date of April 10 (PDUFA date). This early approval aligns with Eli Lilly and Co management’s projection that Foundayo would be approved in “early Q2 2026.”

According to Eli Lilly and Co’s announcement, Foundayo is currently the only GLP-1 oral weight-loss medication that does not require fasting or dietary restrictions on food and drink intake, taken once daily.

Trial data shows that regardless of completion status, participants taking Foundayo achieved an average weight loss of 25 pounds (11.1%), significantly outperforming the placebo group’s 5.3 pounds (2.1%).

Drug and Label Information

Goldman Sachs noted that the FDA’s labeling for Foundayo generally conforms to the existing framework for GLP-1 drugs, with no new risks identified regarding safety or usage restrictions.

The maximum dosage approved for labeling is 17.2mg (once daily), while the highest dosage tested by Eli Lilly and Co in Phase III clinical trials was 36mg.

This discrepancy arises because the commercialized drug uses tablets, whereas the clinical trial used capsules. Tablets are more efficient to produce, use less active pharmaceutical ingredient (API), and are more conducive to large-scale supply.

Eli Lilly and Co has completed the bioequivalence study, confirming that the 17.2mg tablet and 36mg capsule are bioequivalent. The approval of the highest dose means that the efficacy data from the Phase III clinical trial is fully reflected in the labeling.

Pricing Strategy

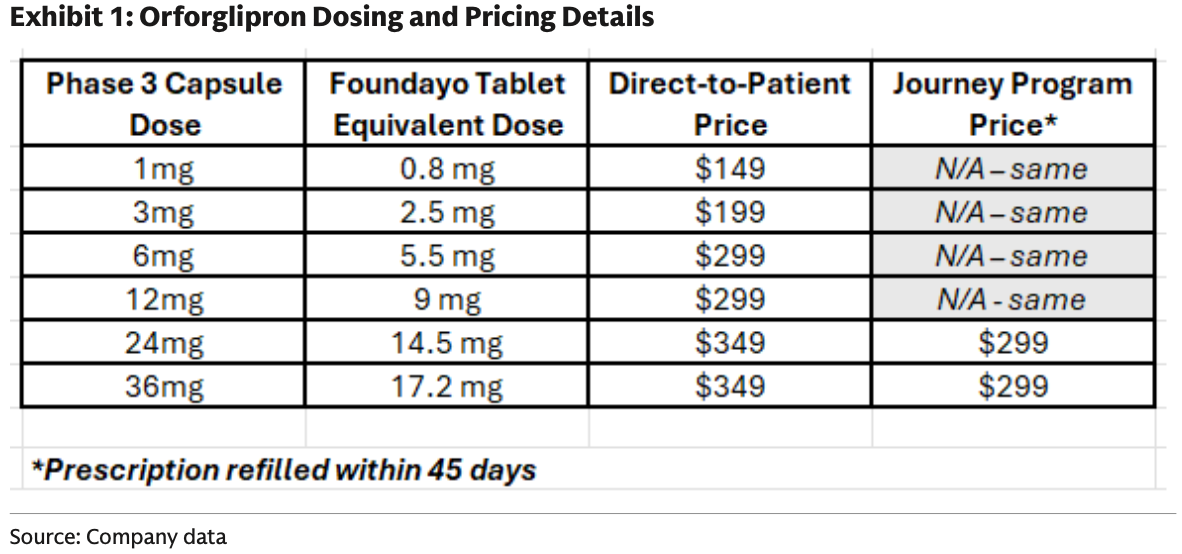

The report indicates that Foundayo’s direct-to-consumer pricing will range from $149 to $349 per month, depending on the dosage.

(Eli Lilly Foundayo Pricing)

Referencing Eli Lilly's previous promotional activities for Zepbound, consumers using higher doses can reduce the monthly price to $299 if they renew their prescription within 45 days.

The price for lower doses (0.8mg to 9mg tablets) will range from $149 to $299 and will not participate in tiered discounts (the price remains consistent).

Sales Forecast and Market Outlook

Goldman Sachs previously assumed that Foundayo would launch in the week of April 17; however, with the drug receiving earlier-than-expected approval, the actual launch will occur sooner, providing more room for sales growth.

According to the median forecast of Bloomberg consensus, Foundayo’s sales this year are expected to reach $1.2 billion. Goldman Sachs believes this target is achievable, and the over one-week early approval provides a buffer for reaching the goal while reducing the risk of missing the target.

Goldman Sachs’ previous (relatively conservative) forecast model showed that Foundayo’s sales in the first 11 weeks would be approximately 50% lower than those of Novo-Nordisk A/S’s oral Wegovy; nonetheless, the annual target can still be achieved.

Novo-Nordisk A/S's oral Wegovy received approval in the United States in late December of last year and officially launched in early January this year.

According to data previously released by Novo-Nordisk A/S, for patients who are obese or overweight and have at least one weight-related complication, their average weight loss was 16.6% after 64 weeks of treatment with oral Wegovy.

In the coming months, investors will focus on the weekly prescription data published by IQVIA. This data covers traditional sales channels and Eli Lilly and Co’s direct sales channel, but initial sales may be underestimated due to the absence of telehealth data, similar to the launch of other new drugs.

Valuation and Investment Rating

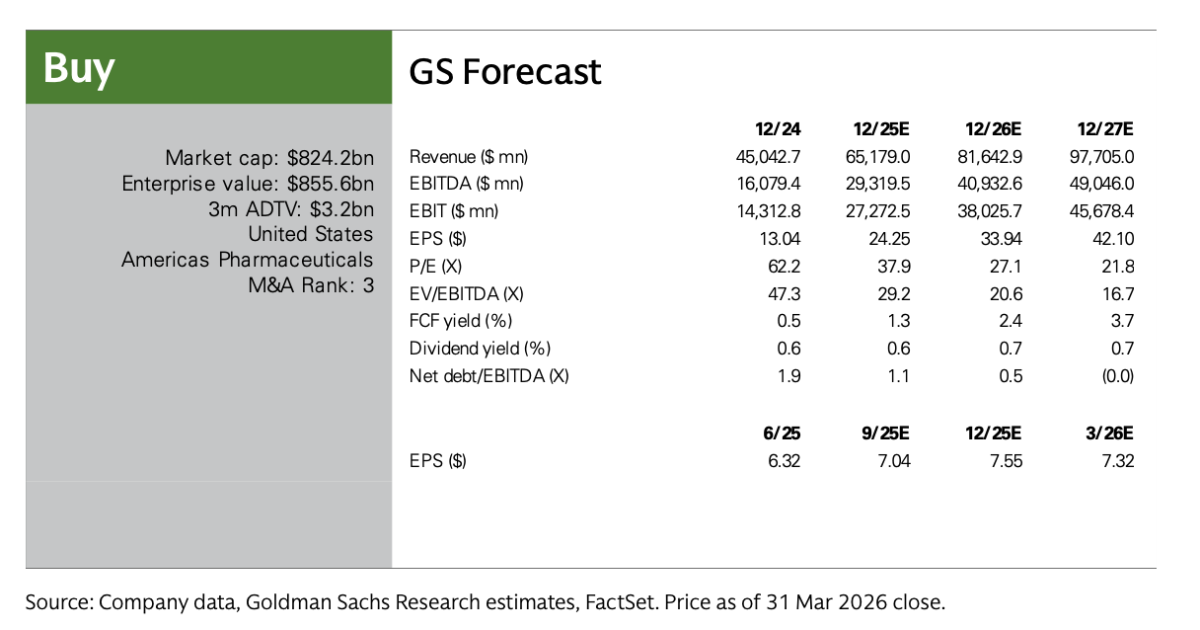

Goldman Sachs analysts maintained a 'Buy' rating for Eli Lilly and Co, with a 12-month target price of $1,260 (based on a P/E ratio of 30x). As of the closing price on April 1 Eastern Time, Eli Lilly and Co’s stock price was $954.52, indicating an upside potential of approximately 32%.

(Goldman Sachs’ revenue outlook for Eli Lilly and Co)

Goldman Sachs expects that Eli Lilly and Co’s total revenue for 2026 will reach $81.643 billion, with EPS (earnings per share) at $33.93; for the full year of 2027, total revenue is projected to be $97.705 billion, with EPS reaching $42.10.

According to analyst forecasts, Eli Lilly and Co’s EBITDA (earnings before interest, taxes, depreciation, and amortization) will continue to grow significantly, increasing approximately threefold from 2024 to 2027, indicating the company is in a high-growth cycle, driven primarily by GLP-1.

Potential risk factors

Goldman Sachs analysts identified three main risk factors facing Eli Lilly and Co.

The first is pricing risk, as annual price reductions in the weight-loss drug market exceed expectations.

Secondly, there is competitive risk, as external competition may intensify (for example, from Novo-Nordisk A/S), or internal execution may be insufficient, leading to a market share lower than expected.

Lastly, there is pipeline risk, where subsequent R&D data falling short of expectations could result in medium- to long-term valuation compression.

Editor/Jayden