The spot price of G652.D bare optical fiber in China has surged by over 400% since May 2025, breaking through the previous cycle's high for the first time. At the same time, prices for similar products in the European market have risen 136% month-on-month compared to January, with the U.S. showing a concurrent upward trend, indicating an increasingly evident tightening of global supply. UBS Group believes that the profits of domestic leader Changfei Optical Fiber have entered an upward revision cycle. The key issue at present is the sustainability of the price rebound and the extent to which the increase in spot prices can be passed on to the company’s profits.

Global optical fiber prices are experiencing a new round of sharp increases, with the upward trend spreading from the Chinese market to Europe and the United States. A surge in data center demand and tightening upstream preform supplies are jointly driving this price cycle, significantly improving the profit outlook for industry leader Changfei Optical Fiber.

According to Trading Wind Platform, UBS Group's latest research report cited the latest data from industry research firm CRU, indicating that the spot price of G652.D bare optical fiber in China reached RMB 83.40 per fiber kilometer (approximately USD 12.07) in March 2026, marking a 165% increase from January 2026 and a year-on-year surge of 418%. Since May 2025, this price has cumulatively increased by over 400%, surpassing the previous cycle's high point of RMB 78.80 per fiber kilometer for the first time. Meanwhile, prices for similar products in the European market have also risen by 136% compared to January, with the tightening global supply becoming increasingly evident.

UBS analysts Jasmine Huang and Sara Wang believe that Changfei Optical Fiber's profitability has entered an upward correction cycle. They significantly raised the company’s earnings forecasts for 2026 to 2028, projecting earnings per share of RMB 4.98 for 2026, far exceeding the market consensus estimate of RMB 1.85.

UBS analysts Jasmine Huang and Sara Wang believe that Changfei Optical Fiber's profitability has entered an upward correction cycle. They significantly raised the company’s earnings forecasts for 2026 to 2028, projecting earnings per share of RMB 4.98 for 2026, far exceeding the market consensus estimate of RMB 1.85.

Chinese optical fiber prices hit record highs, surpassing the previous cycle's gains.

According to CRU's bimonthly report, the spot price of G652.D bare optical fiber in China reached RMB 83.40 per fiber kilometer in March 2026, reflecting a 418% year-on-year increase and a 165% month-on-month rise from January 2026. This represents a further acceleration from the previously reported 92% year-on-year and 79% month-on-month increases as of January 2026.

This price level marks a cumulative increase of over 400% since May 2025 for G652.D bare optical fiber in China, surpassing the previous cycle's high point of RMB 78.80 per fiber kilometer for the first time and setting a new historical record.

Notably, since January 2026, the price of G652.D bare optical fiber in China has surpassed that of similar products in Europe. According to UBS Group's report, the last time this occurred was in November 2018, when large-scale FTTH deployments and 4G network construction in China jointly drove explosive growth in optical cable consumption.

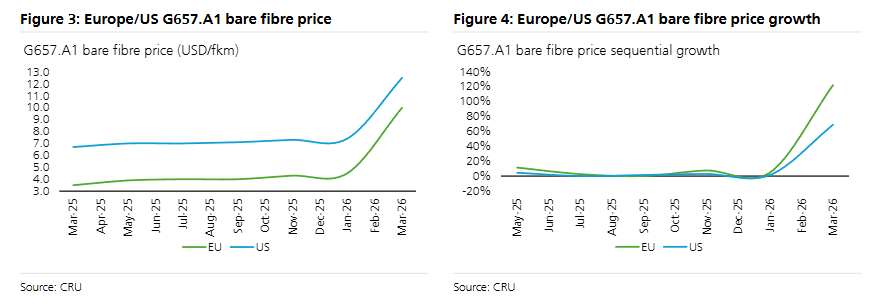

The price surge is spreading to Europe and the United States, with G657.A1 optical fiber showing simultaneous strength.

The rise in optical fiber prices is no longer confined to the Chinese market. CRU data shows that the price of G652.D bare optical fiber in Europe reached EUR 7.94 per fiber kilometer (approximately USD 9.10) in March 2026, representing a 136% month-on-month increase from January 2026 and a 159% year-on-year increase, with the tightening supply effect spreading globally.

Prices for G657.A1 bare optical fiber, used in indoor and bend-insensitive applications, have also risen significantly.

According to CRU data, the month-on-month increase in prices of G657.A1 bare optical fiber in Europe and the United States compared to January 2026 reached 130% and 69%, respectively, primarily supported by strong demand for data communication and tightened supply.

Divergence in Demand Structure: Data Centers Taking Over from Telecom Operators

On the demand side, China and overseas markets exhibit different structural characteristics.

CRU data shows that China’s optical cable consumption remained flat year-on-year in the first quarter of 2026. Demand from telecom operators remained weak, but growth in demand from data centers offset this drag. Optical fiber manufacturers are reallocating capacity toward emerging application areas such as data centers and optical fiber drones. The upstream supply of preforms continues to tighten, while the overall industry expansion remains relatively restrained.

In overseas markets, demand in Yangtze Optical Fiber's core overseas markets (Europe, Southeast Asia, and Latin America) grew by 2% year-on-year in the first quarter of 2026, continuing the 2% growth momentum seen throughout 2025, consistent with UBS Group’s prior assessment of a recovery in overseas demand. The US market performed particularly strongly, with demand growing by 24% year-on-year and 29% quarter-on-quarter in the first quarter of 2026, driven jointly by telecommunications network construction and the expansion of hyperscale data centers.

Significant Upward Revision in Profit Forecasts; Valuation Remains Attractive

UBS Group believes that the sharp rise in spot prices of optical fibers aligns with its channel research results. Yangtze Optical Fiber's profitability has entered an upward correction cycle, supported by improved visibility of optical fiber price increases and product mix upgrades providing sustained support.

In terms of profit forecasts, UBS Group expects Yangtze Optical Fiber’s revenue to grow from RMB 21.062 billion in 2026 to RMB 33.742 billion in 2030, with net profit increasing from RMB 4.122 billion to RMB 8.526 billion. The EBIT margin is expected to rise significantly from 11.4% in 2025 to 24.3% in 2026 and further expand to 32.9% in 2027.

Currently, Yangtze Optical Fiber's share price corresponds to an estimated P/E ratio of approximately 19 times for 2027. UBS Group points out that the key issue investors are currently focused on is the sustainability of the price rebound and the extent to which the increase in spot prices can translate into company profits.

Editor/Jayden