UBS Group noted that the structural trend of gold purchases by official sectors remains unchanged, and central banks will continue to be net buyers of gold despite a slowdown in pace. As concerns over the combination of 'low growth and high inflation' and geopolitical tensions intensify, the medium- to long-term upward trend for gold is strengthening, with the year-end target price maintained at USD 5,600 per ounce.

Since the deterioration of the situation in Iran, the gold market has experienced significant volatility, with gold prices falling 16% in March. Turkey's decision to start selling gold has raised strong concerns in the market about whether the trend of central banks purchasing gold is reversing.

According to the Storm Chaser trading platform, UBS Group’s latest research report clearly pointed out that the structural trend of gold purchases by the official sector has not changed, and central banks will remain net buyers of gold. Although short-term high volatility has led strategic buyers to temporarily adopt a wait-and-see attitude, robust demand from the Chinese market has provided solid support for gold prices.

UBS believes that the current market correction presents an excellent opportunity for investors to establish strategic gold positions. As concerns over the combination of 'low growth + high inflation' and geopolitical tensions intensify, the medium- to long-term upward trend for gold is strengthening. UBS forecasts that the average annual gold price this year will reach $5,000, maintaining a target price of $5,600 by the end of the year.

UBS believes that the current market correction presents an excellent opportunity for investors to establish strategic gold positions. As concerns over the combination of 'low growth + high inflation' and geopolitical tensions intensify, the medium- to long-term upward trend for gold is strengthening. UBS forecasts that the average annual gold price this year will reach $5,000, maintaining a target price of $5,600 by the end of the year.

From Buyers to Sellers? The Panic Over Central Bank Gold Sales Has Been Greatly Exaggerated

The most pressing question for participants in the gold market is: Are central banks selling gold? Particularly in the context of prolonged Middle East conflicts, the market is concerned that central banks may have to sell their gold reserves to address soaring inflation, slowing economic growth, and currency depreciation. This concern is considered the main reason for the 16% drop in gold prices in March.

However, UBS believes that the likelihood of a structural shift in the official sector is extremely low.

UBS expects that central bank gold purchases will only gradually slow down, with estimated purchases of 800 to 850 tons this year, slightly lower than around 860 tons in 2025. During the fifteen-year process of accumulating gold reserves, it is normal for individual central banks to sell gold in certain months. This could be for tactical profit-taking at highly attractive entry levels or due to portfolio rebalancing triggered by rising gold prices.

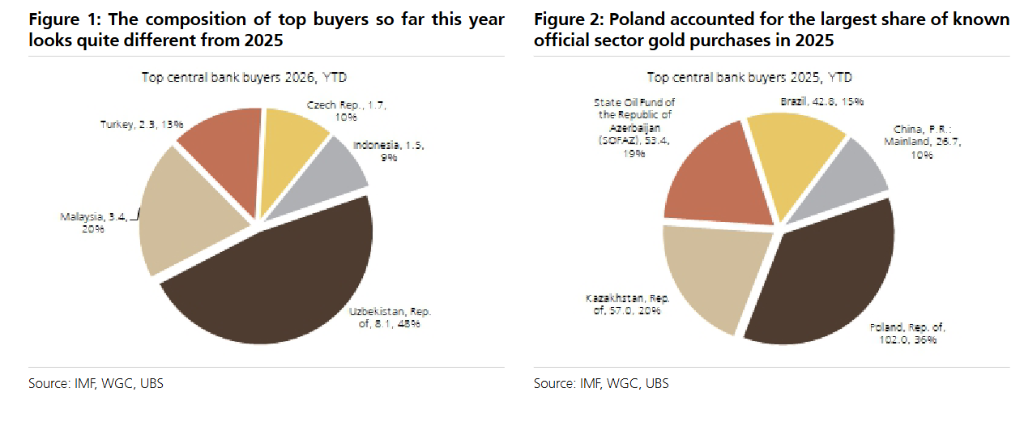

The Truth Behind Turkey’s Sale of 50 Tons of Gold

Recent news reports claimed that the Central Bank of the Republic of Turkey (CBRT) sold approximately 50 tons of gold within a few weeks, drawing significant market attention. However, UBS strongly warned investors against taking these headlines at face value.

Turkey has a unique approach to using gold as a policy tool. Since introducing the Reserve Option Mechanism (ROM) in 2011, part of the total gold holdings reported by the Turkish central bank actually represents positions held by domestic commercial banks. Additionally, some of the reported sales appear to be swap transactions rather than direct sales.

UBS Group noted that there is currently a lag in the data available to break down changes in Turkey's total gold holdings, and the market needs to wait for more detailed data to discern the real trend.

Strategic buyers are temporarily on the sidelines, with demand from China supporting the bottom.

Since 2022, purchases by central banks and official institutions have been a key pillar of the gold bull market. However, recent market flows indicate that the official sector and long-term strategic investors have chosen to stay on the sidelines amid the recent price correction.

The extreme uncertainty triggered by the Middle East conflict in early March, coupled with a sharp rise in U.S. real interest rates and a strengthening dollar, placed heavy pressure on gold prices, leading to liquidation of long positions and short-selling activity.

However, sustained healthy demand from China (with domestic prices remaining at a premium) has helped limit downside risks, allowing the market to stabilize around $4,500. As expectations of Federal Reserve rate hikes reverse, gold prices are now gradually rebounding toward $4,700.

Central Bank Strategy Revealed: Buy-and-Hold Remains the Dominant Approach

To address investor questions about how central banks manage their gold reserves, UBS Group referenced the World Bank’s 'Fifth Biennial Survey of Reserve Managers Report 2025,' published at the end of last year, which covered 136 institutions.

The data reveals the true logic behind central bank gold management:

Decision-making lacks quantification: Most central banks decide on their gold holdings based on “historical considerations” (approximately 47%) and “qualitative assessments” (about 26%), rather than quantitative portfolio optimization models. Only about a quarter of central banks formally incorporate gold into their strategic asset allocation frameworks.

Minimal short-term trading: In terms of investment style, as much as 62% of central banks adopt a “buy-and-hold” strategy. Most crucially, only about 4.5% of central banks indicated they would make short-term tactical adjustments to their gold reserves.

Core driver of增持: Among central banks reporting changes in gold reserves in 2024, more than half cited 'diversification' as the strongest driver for increasing holdings. Other major reasons include local gold purchase programs (approximately 35%) and geopolitical risks (around 32%). Only about 6% of central banks indicated that liquidity needs were a factor in adjusting their positions.

A pullback represents a strategic buying opportunity.

Although gold prices may face further consolidation and volatility in the coming weeks as markets continuously reassess geopolitical risks, UBS Group remains confident in the strong long-term fundamentals of gold.

Speculative positions are currently quite clean, while long-term market participants remain underinvested.

UBS Group emphasized that price pullbacks present an opportunity to establish strategic gold positions. Due to mark-to-market adjustments in the first quarter, UBS Group slightly revised its average annual gold price forecast for this year from $5,200 to $5,000 but firmly maintained the year-end target price of $5,600 set at the end of January.

Editor/Liam