The explosive growth in AI computing power demand is pushing the entire supply chain to its limits. From GPU rentals to DRAM memory, from fiber optic cables to data center hosting, prices have surged across the board in just a few months, while supply remains almost nonexistent.

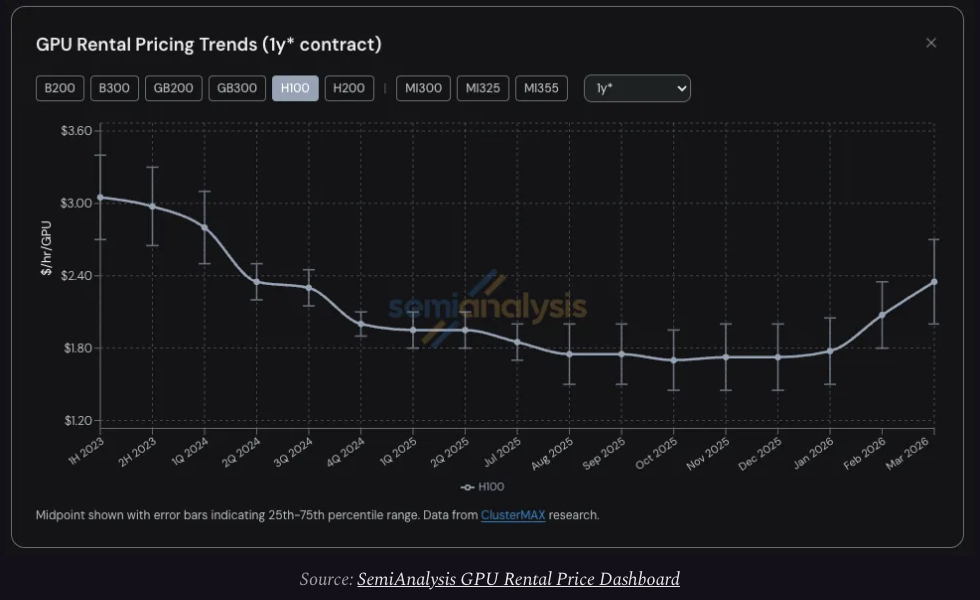

According to the latest report by research firm SemiAnalysis, the price of one-year H100 GPU lease contracts has surged from a low of $1.70 per GPU per hour in October 2025 to $2.35 in March 2026, marking an increase of nearly 40%. Meanwhile, on-demand computing power has been sold out across all GPU models.

The core driver of this round of computing power shortage stems from a structural leap in demand. Anthropic's annual recurring revenue (ARR) skyrocketed from $9 billion to over $25 billion in a single quarter, with workloads like Claude Code driving a parabolic surge in computing power consumption.

SemiAnalysis believes that GPU rental prices are highly likely to continue rising in the short term. Neocloud has begun to take the initiative in pricing negotiations, but$CoreWeave (CRWV.US)$、$NEBIUS (NBIS.US)$the stock prices of related companies such as IREN have not reflected this change.

SemiAnalysis believes that GPU rental prices are highly likely to continue rising in the short term. Neocloud has begun to take the initiative in pricing negotiations, but$CoreWeave (CRWV.US)$、$NEBIUS (NBIS.US)$the stock prices of related companies such as IREN have not reflected this change.

Demand Side: Multi-Faceted Surge, Parabolic Growth in Computing Power Consumption

The demand-side momentum for this round of computing power shortage comes from multiple overlapping directions.

The breakout of Claude Code represents the most significant turning point. Anthropic's ARR surged from $9 billion to over $25 billion in a single quarter, tripling its previous level. The popularity of open-source models such as GLM and Kimi K2.5 further drove up the scale of inference workloads.

At the same time, large-scale financings by AI labs such as Anthropic and OpenAI directly created GPU demand.

AI agents are another key driver. These workloads execute multi-step workflows in high concurrency, continuously iterating, leading to a parabolic rise in computing power consumption.

The native media generation platforms Seedance and Nano Banana have driven a massive demand for computing power in image and video generation scenarios.

From an economic perspective, this demand exhibits significant price inelasticity. SemiAnalysis notes that if the return on investment for AI tools reaches 5 to 10 times, there is still considerable room for GPU rental prices to increase before demand would be curbed.

"The demand curve shifts upward and to the right, providing a strong and relatively inelastic force driving up GPU rental prices."

Supply Side: Surge in Memory Prices Causes Chaos in Server Procurement

The explosion in demand is only one aspect of the computing power shortage; skyrocketing prices on the supply side are another.

January 2026 marks another critical turning point. At that time, the rise in DRAM and NAND memory prices is expected to accelerate. According to SemiAnalysis' memory model estimates, contract prices for LPDDR5 and DDR5 in the first quarter of 2026 are projected to increase by approximately fourfold and fivefold year-over-year, respectively.

The sharp increase in memory prices quickly trickles down to the server end. Original Equipment Manufacturers (OEMs) are repricing AI servers, but the increases significantly exceed the actual rise in component costs.

Higher server procurement costs compress the expected returns on projects, forcing some operators to slow down or even shelve new deployment plans. In other words, the supply originally intended to enter the market has been delayed, further tightening the leasing market.

The supply situation for Blackwell's next-generation GPUs also appears unfavorable. According to SemiAnalysis, delivery timelines for Blackwell’s new clusters have now extended to June-July 2026, primarily due to robust demand for open-source weight models and the ongoing shortage of inference computing power.

Market Structure: Neocloud Gains Pricing Power, Contract Terms Significantly Tighten

The power dynamics of the GPU leasing market have undergone a fundamental shift within six months.

Before the second half of 2025, competition in the market was fierce, with multiple Neocloud companies aggressively undercutting prices to ensure asset utilization rates.

Now, however, Neocloud and hyperscale cloud providers have taken full control — they can not only negotiate higher advance payment percentages, better pricing, and longer contract durations, but also flexibly schedule contract start and end dates based on their inventory conditions.

The GPU leasing market can be divided into three main tiers:

Short-term leases (on-demand, spot, and contracts under three months): typically residual capacity. Currently, such capacity has been entirely sold out, and holders are unwilling to return capacity to the market even in the face of significant price increases.

Medium-term contracts (three months to over three years): the most active segment of market transactions. One-year contracts, in particular, capture marginal demand from non-AI lab customers and serve as the most sensitive indicator reflecting market tightness.

Long-term bulk agreements (four to five years): predominantly led by large AI labs, with individual deals typically reaching sizes of 50 to 100 megawatts or more, equivalent to approximately 24,000 to 48,000 GB300 NVL72 GPUs.

Such deals are highly attractive to Neocloud — long-term contracts allow for favorable debt financing arrangements, locking in double-digit project internal rates of return (IRR), while avoiding GPU price risks. Hyperscale cloud providers sometimes act as guarantors in these deals, further reducing financing costs.

Price Outlook: A Self-Reinforcing Spiral, Yet Neocloud Valuations Remain Undervalued

SemiAnalysis believes that the likelihood of GPU leasing prices continuing to rise in the short term far outweighs the possibility of decline.

The current dynamics exhibit clear self-reinforcing characteristics: tightening supply drives price increases, and rising prices prompt Neocloud to accelerate hardware lock-ins, further tightening supply and causing prices to rise again.

SemiAnalysis compares this to the GPU shortage cycle from 2023 to 2024 but believes that the server market has now matured enough to potentially limit OEMs' ability to achieve excessive profits.

The financial impact of rising rental prices on Neocloud is twofold: on one hand, the profitability of deployed capital expands, improving the return on invested capital (ROIC); on the other hand, higher leasing prices extend the economic service life of existing GPUs, enabling existing assets to generate cash flow for a longer period before reinvestment becomes necessary.

In the current environment, SemiAnalysis believes that Neocloud entities benefiting most prominently possess the following characteristics: shorter contract durations (allowing faster repricing), substantial existing inventories of H100 GPUs, and new capacity coming online in the near term.

However, there is a significant divergence between this fundamental improvement and public market sentiment. The stock prices of listed Neocloud companies such as CoreWeave, NEBIUS, and IREN remain at the lower end of their trading ranges over the past six to twelve months.

SemiAnalysis points out that the market is still dominated by the narrative of 'eventual oversupply and commoditization,' failing to adequately reflect the clearly visible ongoing scarcity and pricing power on the ground.

Three key observation indicators: critical variables determining price trends

SemiAnalysis lists three core observation indicators to assess whether GPU rental prices can remain at high levels.

First, the scaling pace of GB300 clusters. Whether the addition of new computational capacity will alleviate the current shortage or whether the growth rate of computational demand will continue to outpace new supply will determine the extent of AI labs' participation in contracts with terms of less than four years, thereby influencing pricing trends within this segment.

Second, the severity of silicon wafer shortages. SemiAnalysis had previously noted in its reports$Taiwan Semiconductor (TSM.US)$The tight supply of N3 process logic wafer capacity, as well as HBM, DRAM, and NAND memory, implies that complex manufacturing processes carry execution risks at all times.

Thirdly, the growth trajectory of AI lab ARR. The speed of user adoption and the continuous increase in token consumption are the fundamental variables determining the slope of overall demand.

In summary, SemiAnalysis’s conclusion is clear: before the above three indicators show a significant reversal, there is only one direction for computing power prices—upward.

Editor/Liam