On Thursday, the S&P 500 Index rose by 0.11% to close at 6,582.58 points. The Nasdaq Composite Index increased by 0.18%, while the Dow Jones Industrial Average slightly declined by 0.13%. The yield on the 10-year U.S. Treasury bond marginally decreased to 4.30%, and the yield on the 2-year Treasury note remained largely unchanged at 3.80%. The U.S. Dollar Index gained 0.3%. Gold experienced a strong rally this week, maintaining its gains, but fell by 1.8% on Thursday.

Trump delivered a speech to the entire United States without providing any timeline for a ceasefire and issued threats of further strikes on Iran's infrastructure, causing U.S. stocks to drop at the opening. However, news of a draft agreement on the Hormuz Channel changed the intraday trend, allowing the S&P and Nasdaq to narrowly close higher. With Good Friday falling on Friday, U.S. stock markets were closed, marking the first positive week for U.S. equities since the outbreak of the war. WTI crude oil surged over 13% during the day, while U.S. Treasury yields rose before retreating.

Due to certain diplomatic easing signals from the Middle East, market sentiment stabilized somewhat. Investors had previously been unsettled by U.S. President Trump’s threats of stronger action against Iran.

According to reports, Iran and Oman are drafting an agreement aimed at implementing 'passage supervision' for ship transportation through the Strait of Hormuz, while emphasizing that it will not restrict vessel passage. Meanwhile, the UK stated that dozens of countries are discussing plans to end the crisis. These developments alleviated market concerns over a potential prolonged disruption of global oil supplies.

Previously, due to Trump’s hints of potentially more aggressive military actions and with Good Friday approaching (U.S. stock markets would be closed on Friday), rising oil prices triggered market anxiety, causing U.S. stocks to plunge at the opening.

Near-term crude oil futures prices soared significantly, with U.S. WTI crude rising 11% to approximately $111 per barrel, while the international benchmark Brent crude closed up about 7%, nearing $108 per barrel. However, traders priced October oil at around $82 per barrel, indicating market expectations that supply disruptions would be temporary.

Oil price volatility has become a core driver of sharp fluctuations in global stock markets. Since the outbreak of the conflict, equity markets have come under overall pressure, with market movements frequently swinging sharply based on Trump’s statements regarding the progress of the war.

Michael Antonelli, a market strategist at Baird, stated: 'The stock market currently lacks clear direction, but the pricing of October oil reflects the belief that this crisis is likely to end before autumn.'

Market movements on Thursday were almost entirely driven by headlines related to the Strait of Hormuz.

In early U.S. trading, the UK hosted a virtual meeting involving approximately 35 countries to discuss restoring freedom of navigation through the Strait of Hormuz. Subsequently, Iran announced it was drafting a passage agreement for the strait with Oman, causing oil prices to fall significantly and reversing the initial downturn in U.S. stocks, which briefly turned positive.

During midday trading in the U.S., Iranian Deputy Foreign Minister Kazem Gharibabadi stated that passing vessels would need to pay transit fees, causing oil prices to rise again. Later, Trump posted on social media saying, 'It's time for Iran to reach an agreement before it's too late,' pushing oil prices back to their intraday highs.

According to Bloomberg, Cameron Crise pointed out that key details behind Iran's move remain unclear. The specific arrangements for tolls have not been clarified, and it is also uncertain how the U.S. will respond to Iran (in partnership with Oman) taking actual control of one of the world’s most critical waterways. Cameron Crise stated:

From a strategic perspective of the U.S. and Israel, this is clearly an undesirable outcome; but for the White House, a sustained rise in oil prices coupled with a stock market decline represents an equally unacceptable prospect.

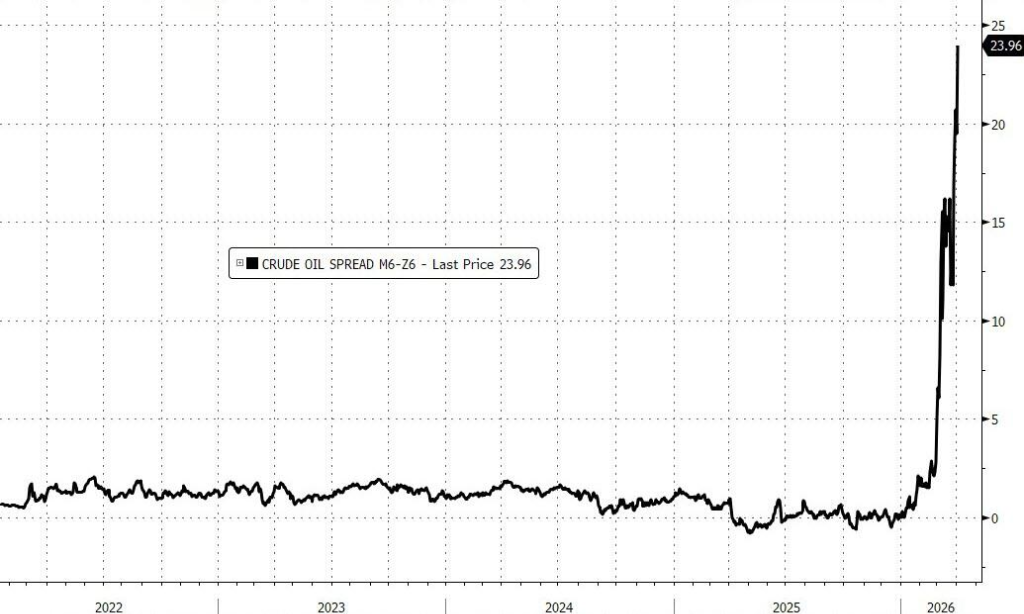

The crude oil market closed the week at its highest level since the outbreak of hostilities. The WTI crude oil futures curve showed a significant backwardation, with the spread between near-term and forward-month contracts hitting a record high.

There is evident divergence in the market’s forecast regarding the duration of the crisis. The futures market indicates that the price of WTI crude oil for October delivery is approximately $82 per barrel. Baird market strategist Michael Antonelli stated:

The October oil price suggests that the market believes this crisis is very likely to end before autumn.

However, institutional views remain relatively cautious. Florian Ielpo, head of macro research at Lombard Odier, stated:

Despite the (optimistic) sentiment, the oil market remains structurally constrained. Even if the conflict ends within weeks, can the disruptions in global energy markets be resolved within the same timeframe? Likely not, thus duration premiums may persist for a longer period.

On Thursday, the S&P 500 Index rose 0.11% to close at 6,582.58 points; the Nasdaq Composite Index gained 0.18%, while the Dow Jones Industrial Average edged down 0.13%.

Data from Goldman Sachs’ trading desk showed overall activity was only rated 2 out of 10 for the day. Long-term funds made small purchases in the information technology, industrial, and financial sectors, while hedge funds continued to offload energy and commodity-related exposures.

This week, U.S. equities recorded their first up week since the outbreak of hostilities, but the quality of the rally has been questioned. Last Friday’s sharp sell-off partially depressed the baseline for the week, making the gains appear more pronounced.

Chris Hussey of Goldman Sachs also pointed out that this week's sharp rebound in the stock market was not based on specific economic data or a ceasefire announcement, but rather driven by news of downgraded expectations. Chris Hussey stated:

The flow through Hormuz has decreased by 13 million barrels per day, and the global economy is still not out of danger.

From a technical perspective, this week’s rebound encountered significant resistance in the range of 6600 to 6700 points. According to SpotGamma data, there is a highly concentrated negative gamma position within this range, with dealers’ hedging flows continuously suppressing upward momentum.

Brendan Fagan of Bloomberg noted that Thursday's high was at 6601 points, which coincidentally touched the lower end of this range, and this was no accident. JPMorgan’s quarterly collar rollover operation also set the upper limit for upward movement near approximately 6800 points, which is expected to create selling pressure during the rebound.

U.S. stocks ended mixed on Thursday, with a significant rise throughout the week, marking the first up week since the Iran conflict; U.S. markets were closed on Friday due to a holiday.

U.S. Equity Benchmark Indices:

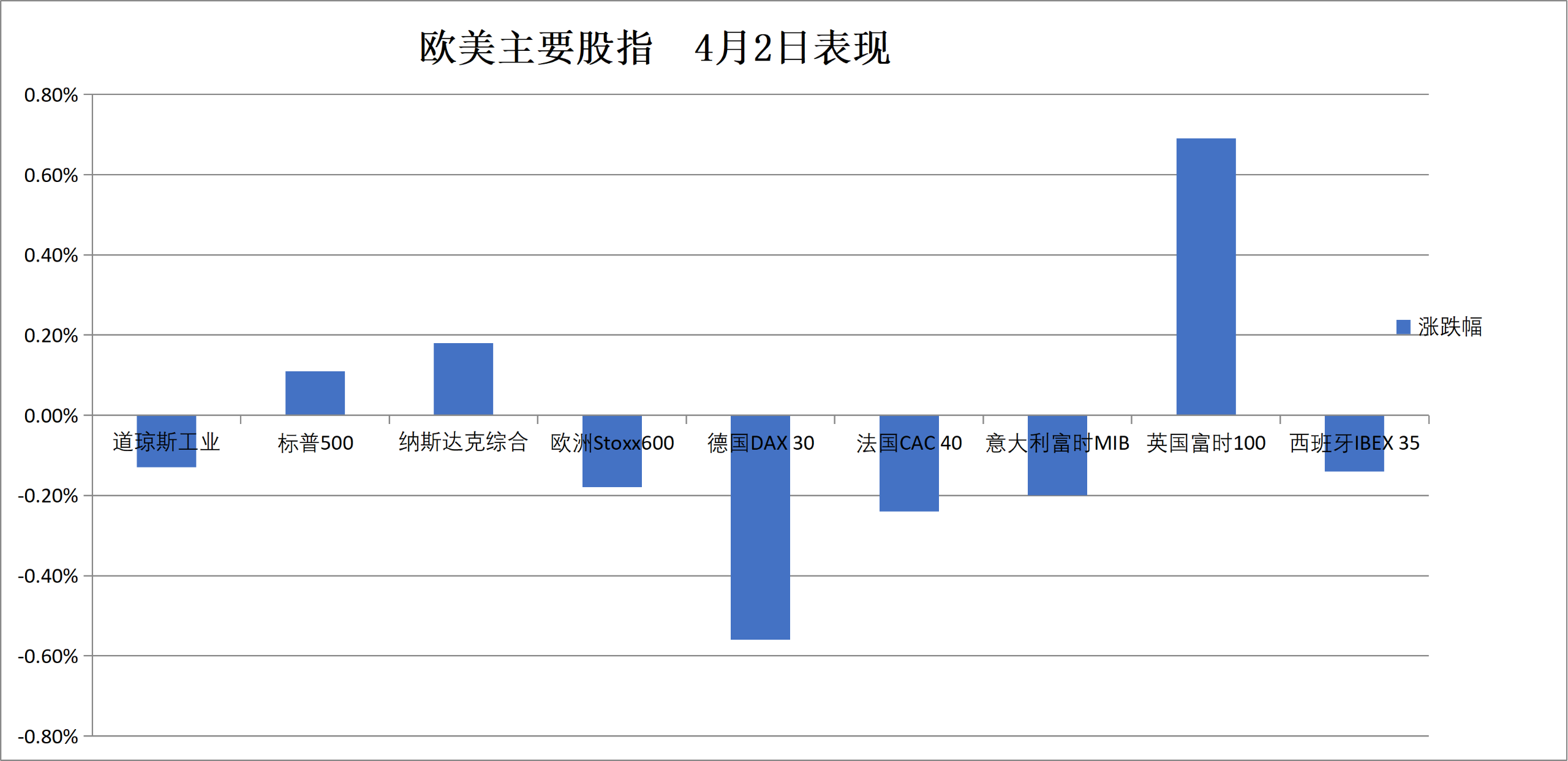

The S&P 500 Index closed up 7.37 points, or 0.11%, at 6582.69 points. After gapping lower at the open, a rapid rebound began at 22:32 Beijing time, with the index remaining slightly down for most of the session. The index has risen 3.36% this week.

The Dow Jones Industrial Average closed down 61.07 points, or 0.13%, at 46504.67 points, with a weekly gain of 2.96%.

The Nasdaq Composite Index rose 38.234 points, or 0.18%, to close at 21879.182 points, gaining 4.45% this week. The Nasdaq 100 Index added 25.545 points, or 0.11%, closing at 24045.532 points, with a weekly increase of 3.95%.

The Russell 2000 Index gained 0.70% to close at 2530.042 points, rising 3.28% this week.

The VIX volatility index fell 2.61% to 23.90, dropping quickly after the U.S. market opened, and declining 23.03% this week.

U.S. sector ETFs:

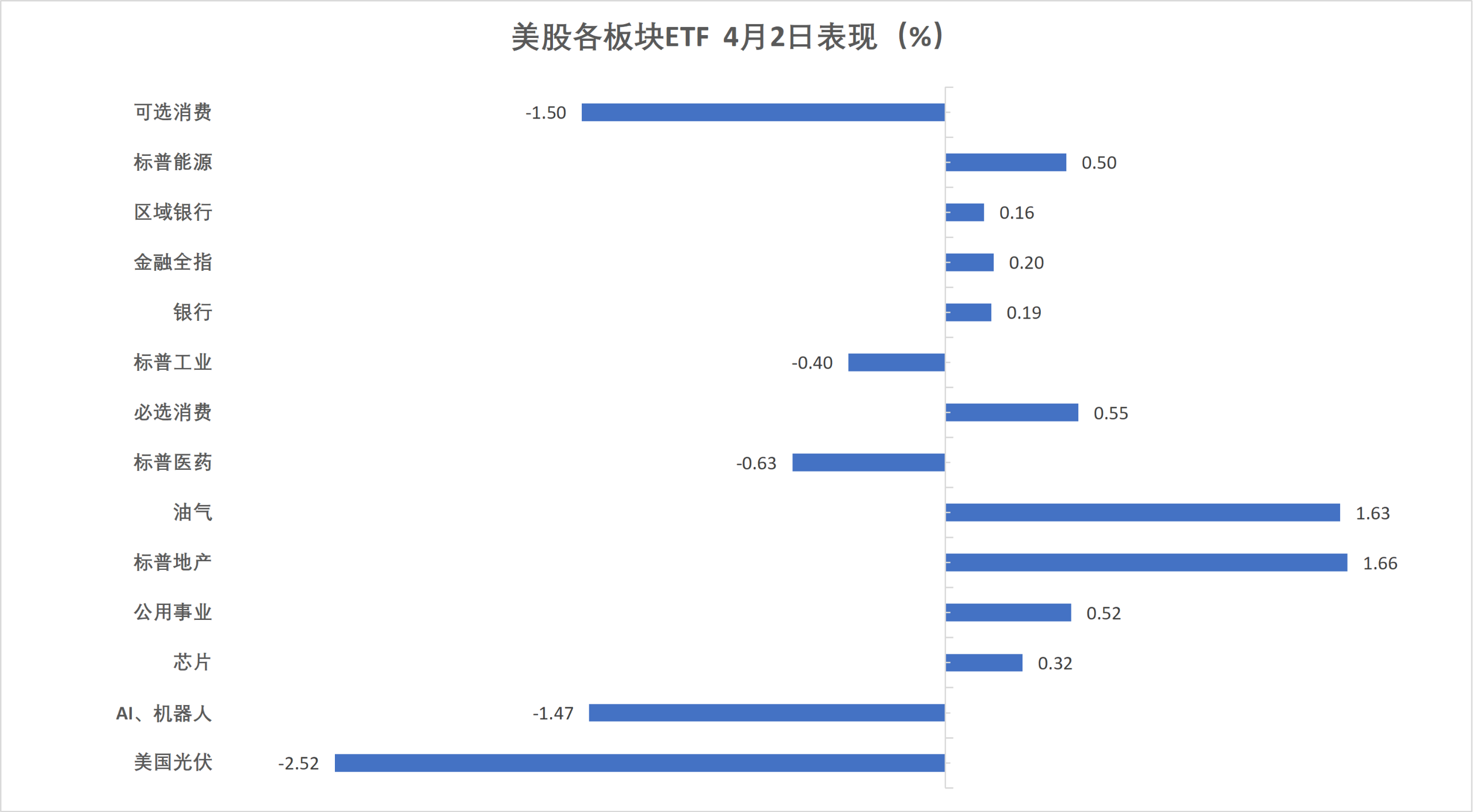

Most U.S. sector ETFs closed higher, with the Internet Index ETF up 1.33%, the Technology Sector ETF gaining 0.82%, the Energy Sector ETF rising 0.47%, the Semiconductor ETF increasing by 0.09%, and the Consumer Discretionary ETF falling 1.50%.

Mag 7:

The Wind Mag 7 U.S. Tech Stock Index fell 0.15%.

Microsoft rose 1.11%, $NVIDIA (NVDA.US)$ up 0.93%, Apple gained 0.11%, while Amazon dropped 0.38%, Google A fell 0.54%, Meta declined 0.82%, $Tesla (TSLA.US)$ down 5.42%.

Semiconductor stocks:

The Philadelphia Semiconductor Index closed up 0.40% at 7833.387 points, having risen 5.04% this week.

$Taiwan Semiconductor (TSM.US)$ fell 0.75%, $Advanced Micro Devices (AMD.US)$ Up 3.47%.

Chinese concept stocks:

The Nasdaq Golden Dragon China Index closed down 0.34% at 6,750.93 points, with a cumulative increase of 2.39% so far this week.

Among popular Chinese stocks, Tencent closed down 2%, while Xiaomi, JD.com, Meituan, Alibaba, and PDD Holdings fell by at least approximately 1%. Li Auto rose 0.4%, XPeng increased by 1.1%, $NIO Inc (NIO.US)$ Up 1.2%.

Other individual stocks:

$Circle (CRCL.US)$ Slightly down 0.55%.

Optical communication concept strengthened, $Lumentum (LITE.US)$ Surged over 8%.

Italy's banking sector closed down 1.9%, but still gained more than 2.7% this week. Germany's stock market rose nearly 3.9%. On Friday, Germany, France, Italy, Greece, Spain, the UK, and others will be closed for holidays.

Pan-European Index:

The STOXX 600 Europe Index closed down 0.18% at 596.63 points, trading narrowly at lower levels for most of the session but quickly recovering losses after 22:30 Beijing time, even turning positive briefly.

The STOXX 50 Eurozone Index closed down 0.70% at 5,692.86 points.

National indices:

Germany's DAX 30 Index closed down 0.56% at 23,168.08 points, with a cumulative gain of 3.89% so far this week.

The French CAC 40 Index closed down 0.24% at 7,962.39 points, with a cumulative gain of 3.38% so far this week.

The UK FTSE 100 Index closed up 0.69% at 10,436.29 points, with a cumulative gain of 4.70% so far this week.

Sector and Stock Performance:

Among the blue-chip stocks in the Eurozone, Deutsche Telekom closed down 3.26%, Infineon Technologies fell 2.96%, Deutsche Bank dropped 2.62%, and UniCredit fell 2.54%, ranking as the fourth-largest decline.

Among all components of the European STOXX 600 Index, Kion Group closed down 9.02%, Valeo Group fell 4.98%, and Taylor Wimpey dropped 4.52%, marking the third-largest decline.

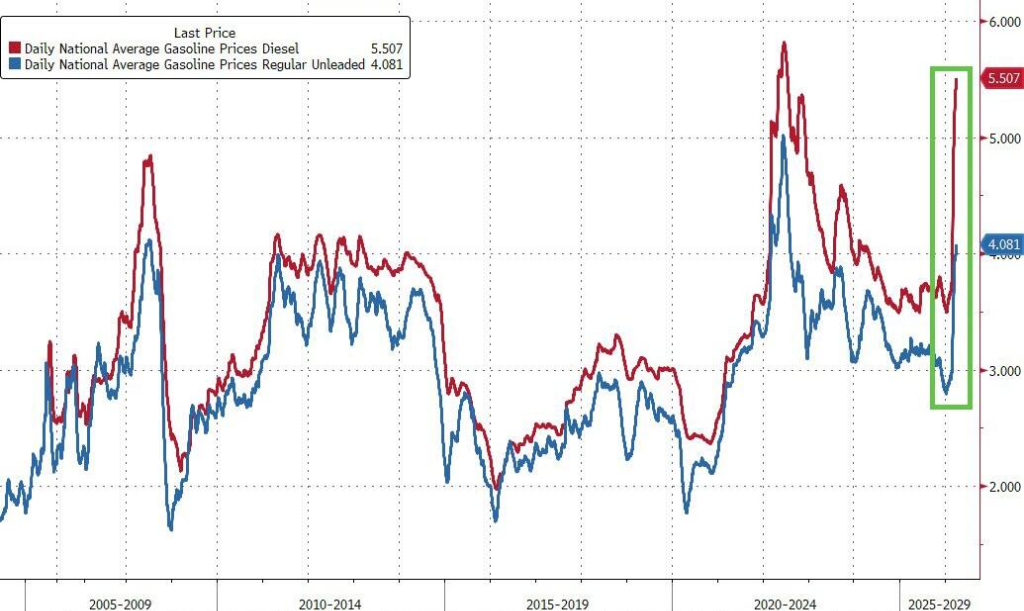

US crude oil futures closed above $110 per barrel for the first time since 2022.

Crude Oil:

WTI May crude oil futures rose by $11.42, gaining over 11.40%, to close at $111.54 per barrel.

Brent June crude oil futures rose by $7.87, gaining nearly 7.78%, to close at $109.03 per barrel.

Middle Eastern Abu Dhabi Murban crude oil futures surged by 9.72% to $113.70 per barrel.

Natural Gas:

The NYMEX May natural gas futures contract closed at $2.8 per million British thermal units (MMBtu).

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/Stephen