Amid the explosive growth in global demand for artificial intelligence (AI) industries, the shortage of GPU computing power has further intensified, leading to a significant surge in the rental prices of core computing chips.

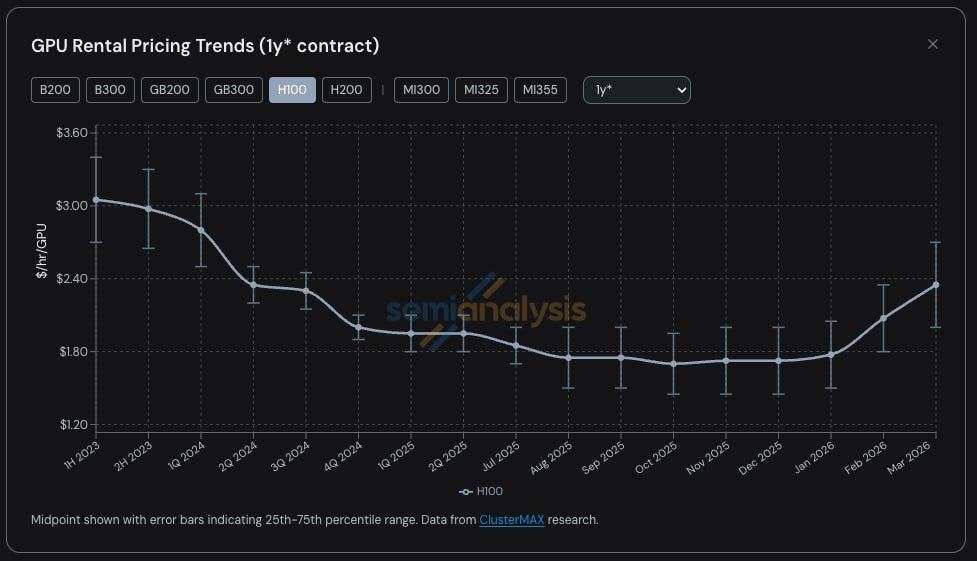

According to the latest data released by industry research firm SemiAnalysis,$NVIDIA (NVDA.US)$The one-year lease price for the H100 GPU has surged significantly. As of March 2026, the annual contract rental rate has risen from $1.70 per GPU per hour in October 2025 to $2.35, reflecting an increase of nearly 40%. The entire industry’s GPU computing resources have been almost entirely sold out.

H100 lease prices rose nearly 40% in six months; the spot market is under severe pressure.

Index data released by SemiAnalysis shows that the current surge in H100 lease prices began in Q4 2025, with momentum accelerating notably into 2026. By the end of January 2026, the annual contract price for the H100 first exceeded the $2 per hour per card threshold, and the month-on-month increase in February reached 15%-20%.

By the end of March, prices had climbed to $2.35 per hour per card, representing a near-40% increase from the low point six months earlier, with the month-on-month increase for March expected to remain at a high of 15%-20%.

By the end of March, prices had climbed to $2.35 per hour per card, representing a near-40% increase from the low point six months earlier, with the month-on-month increase for March expected to remain at a high of 15%-20%.

The supply-demand tension in the spot market is even more extreme. The report notes that on-demand rental capacity for all types of GPUs has been completely sold out. Even as prices continue to rise, users who have secured on-demand instances are unwilling to release their capacity back into the market. SemiAnalysis commented that at the beginning of 2026, the difficulty of purchasing GPU computing power in the market was comparable to scrambling for last-minute flight tickets during peak season—not only were prices high, but available spot resources were almost entirely depleted.

SemiAnalysis also noted that extreme supply-demand imbalances have led to numerous unconventional phenomena in the market. Some users are willing to pay up to $14 per hour per card to access AWS's p6-b200 spot instances, while leading new cloud providers have ceased selling single-node computing power. Many H100 lease contracts signed 2-3 years ago are being renewed at their original prices, with some contracts even extending directly to 2028 to lock in long-term capacity. Additionally, some computing power tenants are splitting and subleasing their rented clusters, similar to premium apartment rentals during major sporting events.

Full-series chip supply remains tight, with widespread price increases across the value chain.

This price surge has not been limited to older-generation chips.$NVIDIA (NVDA.US)$The newly launched Blackwell series GPUs are also experiencing supply shortages. Driven by strong demand, delivery timelines for the new chips have been extended to June-July 2026, and all production capacity scheduled to go online in August-September 2026 has already been fully pre-booked.

Notably, the market had previously anticipated that the arrival of the more energy-efficient new-generation chips would drive down prices for older models like the H100. However, the reality has been the opposite, with demand for older GPUs remaining consistently high or even strengthening further. The H200 chip, which belongs to the same Hopper architecture, is also facing supply exhaustion. Procuring an 8-node (64-card) cluster of H100 or H200 has become extremely difficult. SemiAnalysis’s survey of suppliers revealed that half reported related capacities were completely sold out, and most manufacturers confirmed they had no Hopper architecture GPU contracts expiring soon to release additional capacity.

The surge in upstream industry prices has further exacerbated the tightness in computing power supply. The report points out that January 2026 became a critical turning point for memory prices. DRAM and NAND flash prices, which had been rising sharply for several consecutive quarters, saw parabolic spikes in the first quarter of 2026. According to SemiAnalysis’s memory model estimates, LPDDR5 and DDR5 contract prices in the first quarter of 2026 are projected to increase year-over-year by approximately fourfold and fivefold, respectively.

The surge in prices of core components such as memory has driven up the overall cost of AI servers. To hedge against gross margin risks, server OEMs have significantly raised AI server quotations, with increases far exceeding the rise in component costs. This has directly compressed the expected returns of computing cluster projects, forcing many operators to slow down or even abandon plans for deploying new clusters. New supplies that should have entered the market have been shelved, further tightening the supply dynamics in the leasing market.

A comprehensive surge in demand has been the core driver of the current computing power shortage. On one hand, companies like ByteDance$Alphabet-A (GOOGL.US)$The rapid proliferation of media-generation AI tools by enterprises such as Anthropic's Claude 4.6 Opus and Claude Code has led to a surge in demand for these models, with their annual recurring revenue (ARR) skyrocketing from $9 billion to over $25 billion in a single quarter. This growth is further compounded by the explosive increase in usage of open-source models like GLM and Kimi K2.5, alongside significant capital raises by AI companies such as OpenAI and Anthropic, which have subsequently driven up GPU procurement needs.

On the other hand, the scaled application of multi-agent workflows has resulted in exponential growth in token consumption. The exceptionally high return on investment of AI tools has created strong rigidity in computing power demand, further widening the supply-demand gap.

The market structure is undergoing profound restructuring, with upward price pressure expected to persist in the short term.

Regarding future market trends, the report highlights a clear divergence between secondary market sentiment and fundamental industry conditions. Despite tightening GPU supply and significant price increases, which directly benefit new cloud providers through margin expansion and extended asset lifespans, the secondary market remains persistently pessimistic toward leading new cloud vendors.$CoreWeave (CRWV.US)$、$NEBIUS (NBIS.US)$、$IREN Ltd (IREN.US)$Relevant company stock prices have fallen to the lower end of their 6-12 month trading range.

The market remains anchored to the narrative that 'GPUs will eventually become oversupplied and commoditized,' starkly contrasting with the ongoing shortages and increasing pricing power observed among manufacturers.

SemiAnalysis notes that the future trajectory of GPU rental prices hinges on three critical milestones that warrant close monitoring:

The progress of the large-scale implementation of the GB300 cluster in 2026 will be observed to determine whether the increase in computing power supply can alleviate the current shortage or if the growth in token demand continues to outpace new supply.

Whether the shortages in the semiconductor supply chain will worsen further, with a particular focus on capacity constraints in key areas such as Taiwan Semiconductor's (TSM.US) N3 advanced process, HBM, and DRAM/NAND memory.

The ARR growth rhythm of AI laboratories and the growth rate of token consumption driven by the widespread adoption of AI tools.

In summary, SemiAnalysis provides a clear assessment in its report: underpinned by multiple factors, GPU rental prices are highly likely to continue rising. This trend has formed a self-reinforcing cycle—anticipating tightening supply and rising prices, new cloud providers are locking in more hardware capacity in advance, further exacerbating supply constraints and pushing prices higher.

This round of price increases will directly enhance the return on deployed capital for new cloud vendors while extending the economic service life of existing GPUs. Vendors with a high proportion of short-term contracts (which can be repriced quickly), a large installed base of H100s, and recently added production capacity will become the most direct beneficiaries.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/Melody