①The U.S. Bureau of Labor Statistics (BLS) will release the March figures at 8:30 PM Beijing time tonight.Nonfarm payroll data②As the first U.S. non-farm payroll report covering the impact of the Middle East conflict, investors will undoubtedly scrutinize the detailed data in the employment report to assess the Federal Reserve's specific interest rate trajectory later this year.

The Bureau of Labor Statistics (BLS) will release the non-farm payroll data for March at 8:30 PM Beijing time tonight. As the first U.S. non-farm report covering the impact of the Middle East conflict, investors will undoubtedly scrutinize the detailed data in the employment report to assess the Federal Reserve's specific interest rate trajectory later this year.

It is worth noting that due to the Good Friday holiday, the U.S. stock market will be closed tonight, so the full impact of the non-farm data release may not be fully reflected until next Monday. Of course, the foreign exchange and bond markets will still be trading normally tonight when the non-farm data is released. In the low liquidity holiday atmosphere, traders in the bond and currency markets may need to be more vigilant about market volatility being amplified.

How is the market expecting tonight’s non-farm data to perform?

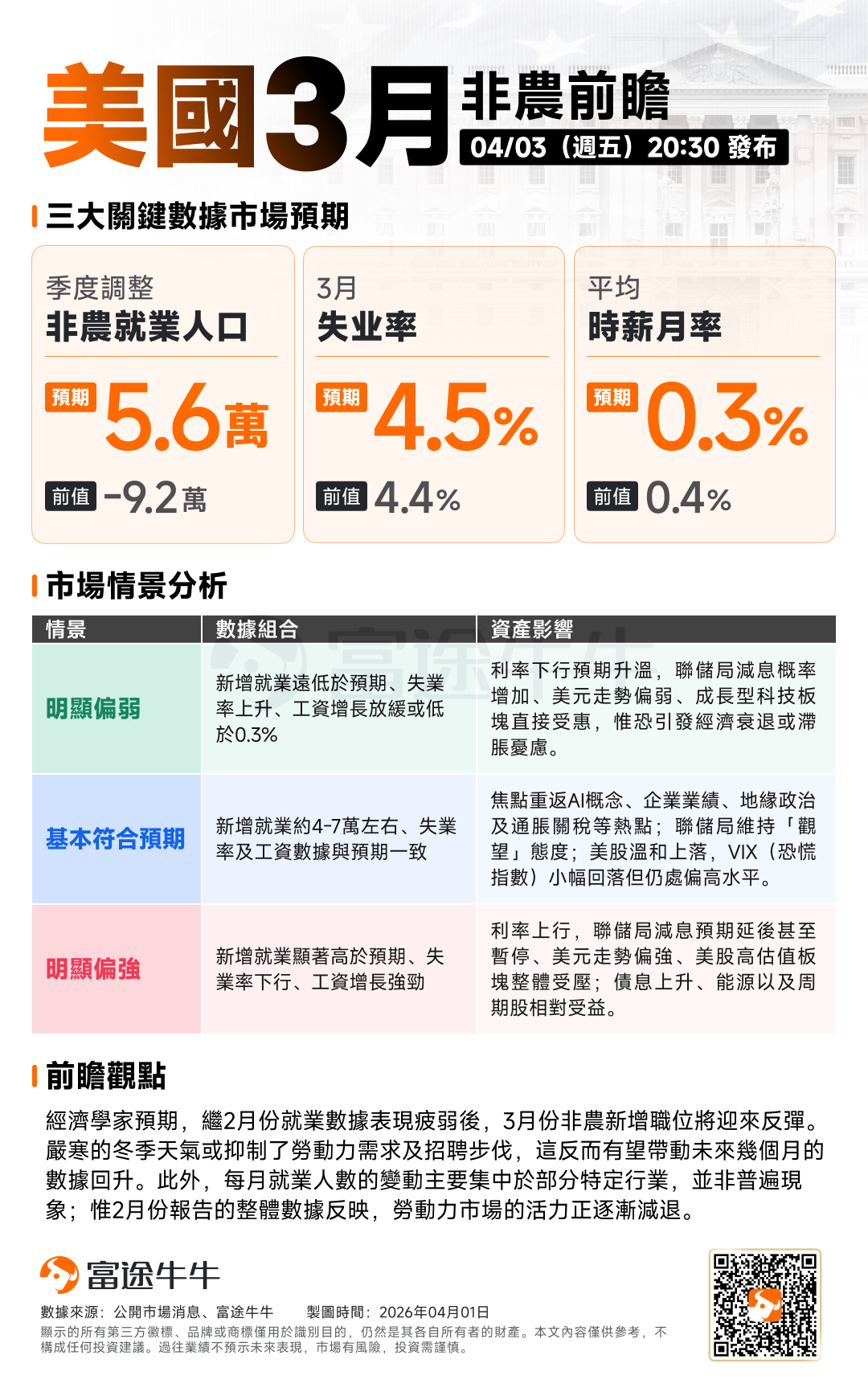

According to a survey of economists by the media, the number of new non-farm jobs in the U.S. in March is expected to reach 60,000, reversing the unexpected decrease of 95,000 positions in February caused by a large-scale strike among healthcare workers.

According to a survey of economists by the media, the number of new non-farm jobs in the U.S. in March is expected to reach 60,000, reversing the unexpected decrease of 95,000 positions in February caused by a large-scale strike among healthcare workers.

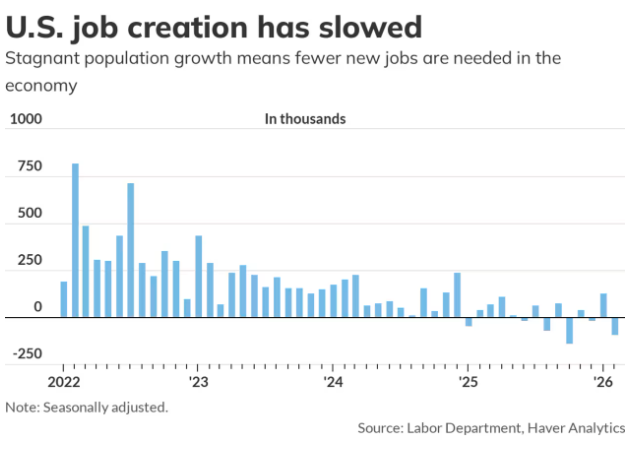

If the data meets expectations, this monthly increase will be roughly on par with that of March last year, and it may be sufficient to reach the current 'break-even point' of the U.S. job market — the number of jobs needed to maintain a stable unemployment rate amid a sharp decline in immigration.

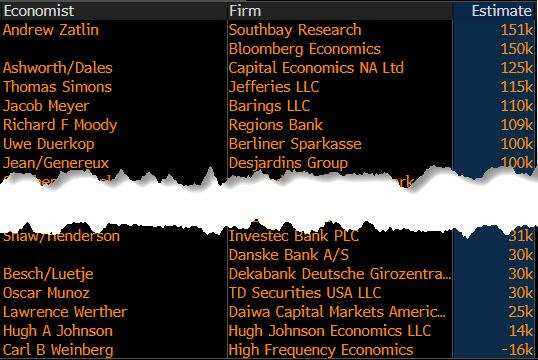

Currently, Wall Street institutions have significant differences in their forecasts for tonight's data — the most optimistic estimate suggests a growth of 150,000 in non-farm employment in March, while the most pessimistic predicts a reduction of 15,000, marking the second consecutive month of 'negative non-farm'.

Regarding the unemployment rate, economists expect the U.S. unemployment rate in March to remain stable at 4.4%. Although by past standards, a 'mid-single digit' level increase in U.S. non-farm data in a given month would appear quite weak, nowadays such figures might already be sufficient to keep the U.S. unemployment rate stable, or even be considered a decent data performance.

Guy Berger, chief economist at Homebase, which provides labor management services for small businesses, stated: 'We must readjust our understanding of what constitutes good or bad employment data.'

At the press conference following last month’s Federal Reserve decision, Chairman Powell mentioned that the breakeven point for U.S. job growth is currently low. The figure previously cited by the Fed was approximately 50,000, but he suggested it could now be as low as zero, which is reasonable given the collapse in illegal immigration (affecting both the numerator, employment numbers, and the denominator, labor force size).

It should be noted that the volatility of the US non-farm payrolls reports over the past two months has been significant — with a strong addition of 126,000 jobs in January (much stronger than expected), followed by an unexpected loss of 92,000 jobs in February. Therefore, how the upcoming non-farm payrolls report revises the data for the previous two months will be a major focus for market participants.

Could the exceptionally weak February non-farm payrolls be distorted?

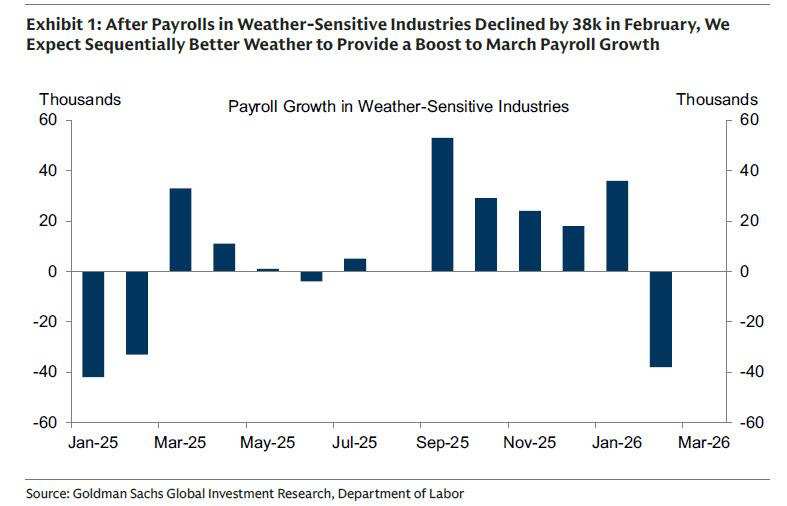

Overall, industry insiders generally believe that the non-farm payrolls figure showing a loss of 92,000 jobs in February is indeed very disappointing — but there may be some distortions behind it: approximately 30,000 workers from Kaiser Permanente and Starbucks were on strike at the time and not counted in the labor force, while harsh winter weather severely impacted the construction sector as well as leisure and hospitality industries.

If these two factors are excluded, underlying job creation actually approached a decline of around 30,000 to 40,000 positions. While still weak, it would not appear as extreme.

When forecasting the March non-farm payrolls, many investment banks currently expect that several negative factors affecting February’s employment data may ease, potentially even boosting the performance of March figures to some extent. Analysts at TD Securities pointed out that they anticipate a moderate increase of 30,000 in non-farm payrolls for March.

"The reversal of weather and strike impacts should lead to an employment composition similar to late 2025, with substantial support this month coming from the healthcare sector. We also expect the unemployment rate to remain at 4.4%, although there is an upside risk. Average hourly earnings may see a modest month-on-month growth of 0.2%, translating to an annual increase of 3.6%," TD Securities added.

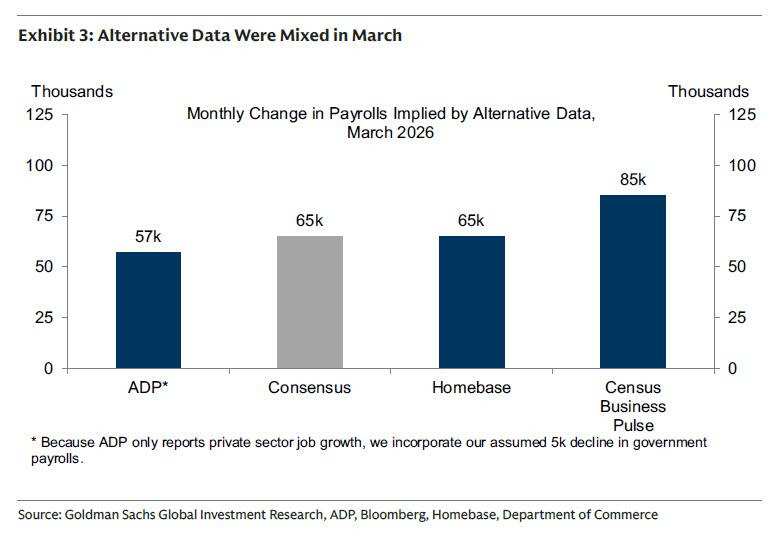

Automatic Data Processing (ADP) reported earlier this week that private-sector employment increased by 62,000 in March. Nela Richardson, Chief Economist at ADP, commented on the report, stating that overall hiring remained stable, while monthly job growth was skewed toward certain sectors, including healthcare (which saw a sharp decline in February).

Goldman Sachs estimates that March’s new non-farm payrolls will slightly exceed market consensus expectations, reaching 70,000.

Goldman Sachs identified positive factors for non-farm payrolls, including a boost of 32,000 jobs due to the end of worker strikes; seasonal warming following February's adverse weather; and a decrease in the average number of initial unemployment claims in March to 211,000, down from 220,000 in February.

On the downside, Goldman Sachs expects government employment to decline by 5,000 (a reduction of 10,000 in federal government jobs, partially offset by an increase of 5,000 in state and local government positions).

The mixed/neutral factor was the mixed signals from other indicators measuring employment growth in March. The employment indicators tracked by Goldman Sachs on average suggested an employment growth of 69,000 people in March.

Is the impact of the Middle East conflict still limited for now?

As the first non-farm payroll report under the impact of the Middle East conflict, many investors tonight are also interested in understanding how much this conflict has affected the U.S. labor force. However, industry insiders generally believe that it is still too early to judge how much the conflict will affect the fragile U.S. labor market, and at least the March report is unlikely to show significant impacts.

Nancy Vanden Houten, chief economist at Oxford Economics, stated in a report on Thursday: 'The war between the United States/Israel and Iran has made the labor market more vulnerable, but any impact will take time to materialize. The latest unemployment claims data confirm this, as these figures indicate stable labor market conditions.'

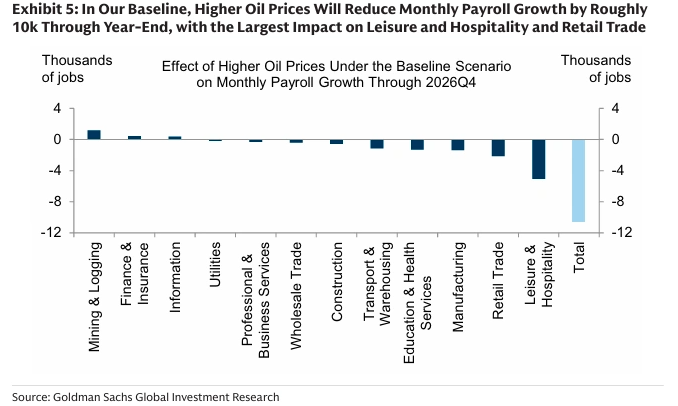

Goldman Sachs is currently the only institution that has explicitly modeled the impact of oil shocks on the labor market — the bank estimates that by the end of the year, U.S. employment will be dragged down by an average of about 10,000 people per month, mainly concentrated in the leisure and hospitality industries and retail, as energy costs erode household real income.

However, Goldman Sachs pointed out that the key lies in the lag time of the conflict's impact, which often ranges from four to eight weeks. Hiring during the March non-farm survey period mainly reflected sentiment from late February to early March — therefore, the March data may appear decent, while the real damage might become evident in April and May.

Of course, given that the Middle East conflict has already caused market expectations regarding the Fed’s interest rate path to swing between rate hikes and cuts, the performance of tonight’s non-farm data will largely continue to influence the tilt of the Fed’s interest rate balance.

From an interest rate pricing perspective, prior to the outbreak of the U.S.-Iran conflict on February 28, overnight index swaps (OIS) had priced in more than two Federal Reserve interest rate cuts (each by 25 basis points) for this year. These expectations were subsequently erased due to inflation concerns, and traders began pricing in the possibility of the Fed’s next move being a rate hike. However, recently, the market has started repricing toward the view that the Fed may be closer to cutting rates again.

Tom di Galoma, Managing Director at Mischler Financial Group, stated, 'This non-farm payroll data is highly likely to exceed bond market expectations. Throughout the week leading up to the long Easter holiday weekend in the UK and Europe, risk aversion and position unwinding have been underway.'

The Fxstreet analyst team noted that if the non-farm employment number shows an unexpectedly strong performance above 70,000, it may prompt the market to reassess the possibility of a Fed rate hike and boost the U.S. dollar. Conversely, if the data falls below 50,000, especially accompanied by a rise in the unemployment rate, the U.S. dollar may struggle to outperform other currencies.

Stay ahead with key financial updates and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Stay ahead with key financial updates and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Editor/Doris