Zheshang Securities pointed out that the recent sharp decline in gold prices is primarily due to short-term liquidity disruptions, which are now coming to an end. Turkey’s sale of gold has a highly unique background: gold accounts for nearly half of its reserves while its holdings of U.S. Treasuries are minimal, forcing it to sell gold to pay for energy imports. In contrast, European countries hold significant gold reserves, but as gold underpins the credibility of the euro, there is little incentive for them to sell. Gold benefits from both scenarios: Rising geopolitical tensions lead to higher oil prices and recessionary trading, strengthening expectations for interest rate cuts; easing tensions result in lower oil prices, opening up room for rate cuts. Both pathways are favorable to gold.

The ongoing escalation of conflicts in the Middle East and persistently high oil prices have led to an unusual sharp decline in gold amid this round of geopolitical tensions. However, this abnormal performance does not signify a collapse in fundamental logic but is instead attributed to short-term liquidity disruptions, which are now showing signs of easing.

In its latest monthly report, Zheshang Securities pointed out that gold is likely to benefit regardless of whether geopolitical tensions escalate or ease. This "two-way benefit" logic makes gold a rare asset with significant allocation value in the current chaotic market environment.

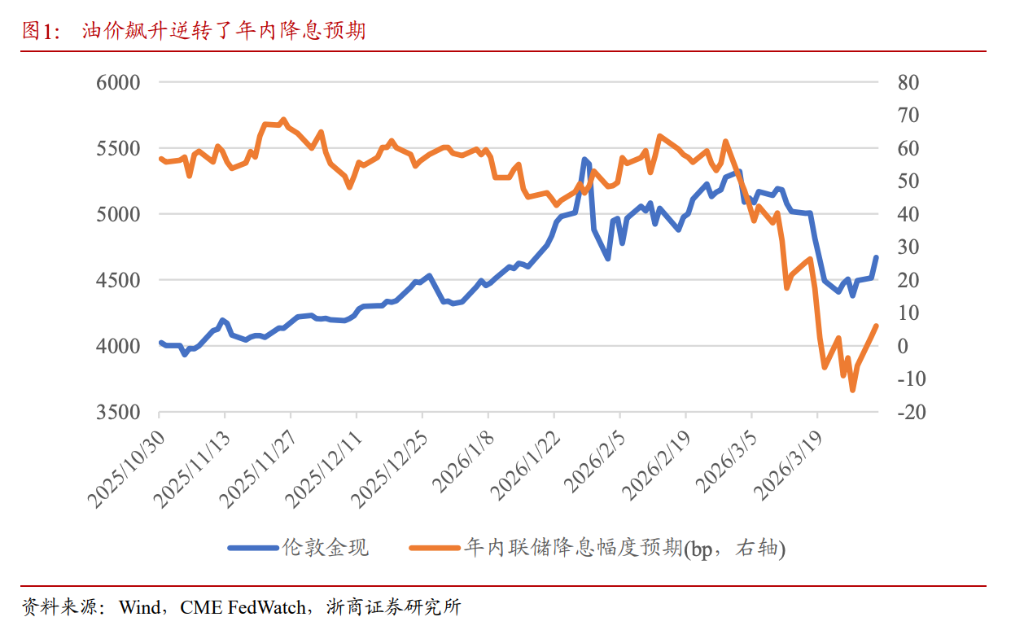

Specifically, the market previously followed the trading logic of "rising oil prices → rollback of rate-cut expectations." However, the report notes that if oil prices remain high for more than a quarter, the demand destruction effect will begin to manifest, significantly weakening the economic fundamentals. In other words, the higher the oil price, the greater the risk of recession, which could paradoxically lead to a rise in rate-cut expectations. With the conflict having lasted for a month, the turning point from 'rate-hike trades' to 'recession trades' may be imminent.

Specifically, the market previously followed the trading logic of "rising oil prices → rollback of rate-cut expectations." However, the report notes that if oil prices remain high for more than a quarter, the demand destruction effect will begin to manifest, significantly weakening the economic fundamentals. In other words, the higher the oil price, the greater the risk of recession, which could paradoxically lead to a rise in rate-cut expectations. With the conflict having lasted for a month, the turning point from 'rate-hike trades' to 'recession trades' may be imminent.

Meanwhile, the trend of global central banks increasing their gold reserves remains unchanged. Turkey's sale of gold is an isolated case due to its heavy reliance on energy imports, high gold reserves, and minimal holdings of U.S. Treasuries, making it a forced financing measure for oil imports. Major European countries have maintained stable gold reserves over the long term, which also serve as a credit endorsement for the euro, leaving them with little motivation to reduce their holdings.

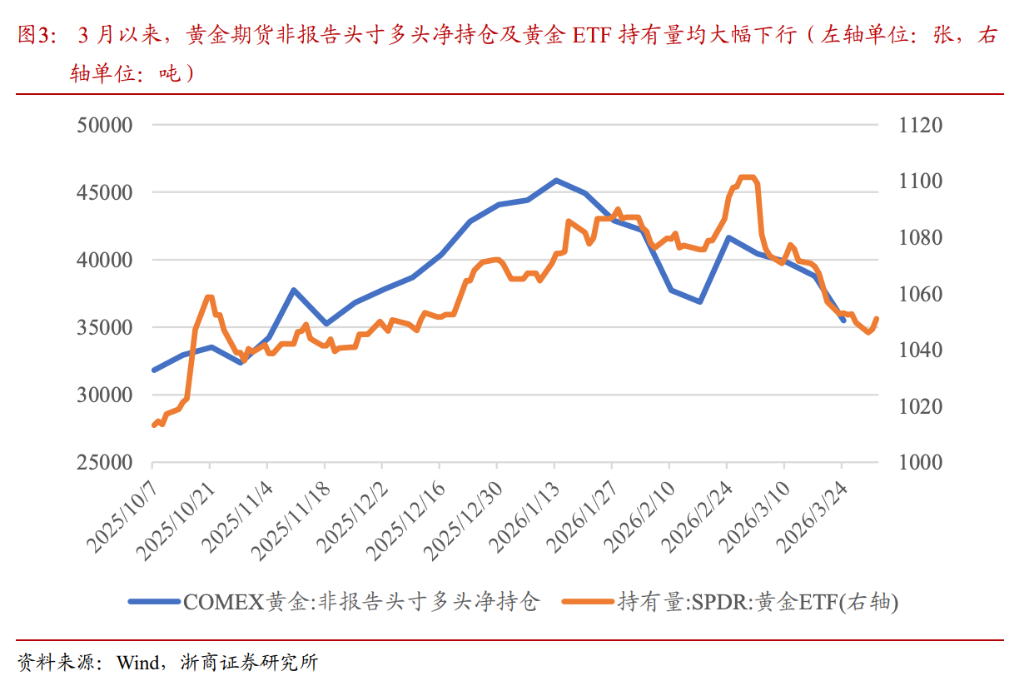

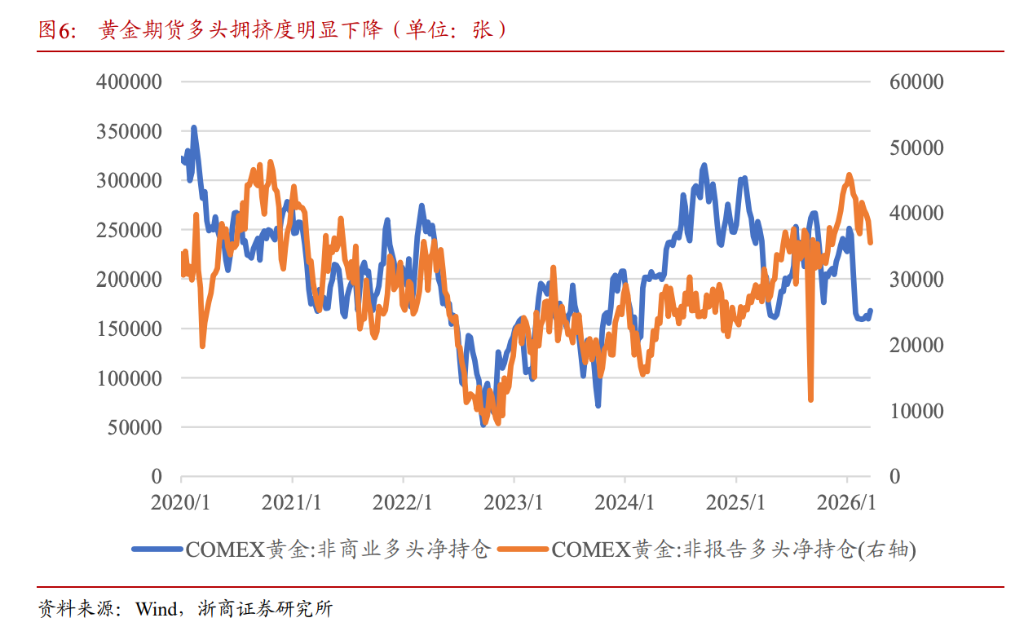

Additionally, improvements in position structures have provided conditions for gold to return to fundamental pricing. Currently, both net long positions of non-commercial traders in COMEX gold and retail investor positions have significantly declined compared to previous levels, indicating that liquidity-related pressures on gold are nearing an end.

Why Did Gold 'Fail' Amid Geopolitical Conflicts? Liquidity Is the Real Culprit

Historically, the loss of gold's safe-haven status often occurs during periods of liquidity crises, such as during the 2008 financial crisis and March 2020. Similarly, the sharp initial decline in gold during this round of Middle East conflicts can be attributed to liquidity disruptions, specifically stemming from three layers of liquidity pressures:

First, surging oil prices reversed rate-cut expectations, leading to an overall contraction in global liquidity. As oil prices surged rapidly, rate-cut expectations for the year were quickly withdrawn, and by around March 20, the market even began pricing in rate hikes within the year, directly tightening the global liquidity environment and pressuring gold.

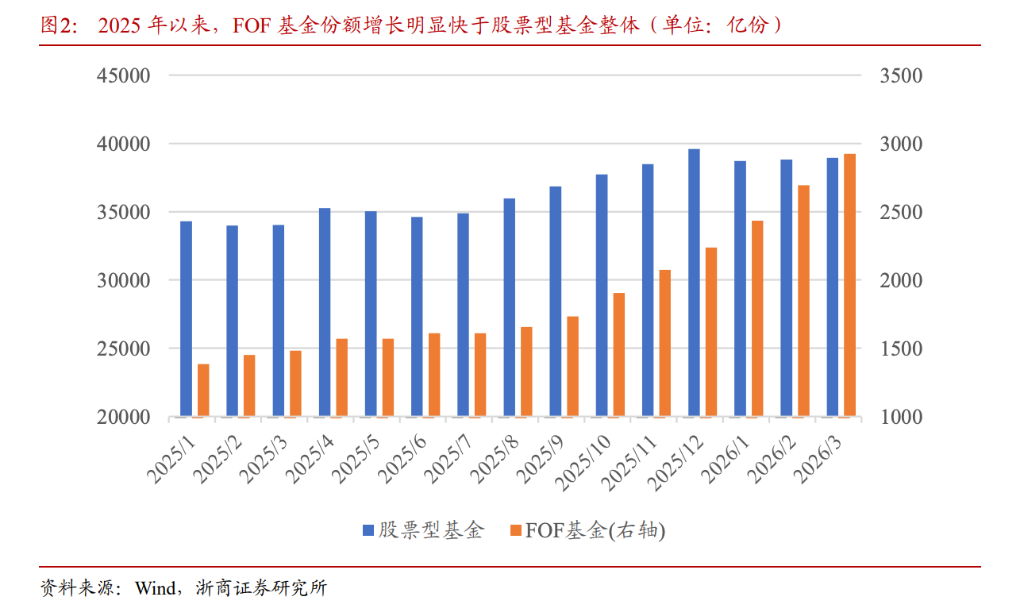

Second, the expansion of multi-asset strategy funds triggered systematic deleveraging under tail-risk scenarios. The broad-based rally in global assets in 2025 fueled rapid growth in multi-asset strategies (such as FOFs). Data shows that between January 2025 and March 2026, equity fund shares increased by 13.6%, while FOF fund shares surged by 111.2%. When tail risks emerged, systematic deleveraging across multi-asset strategies caused the unusual phenomenon of synchronized declines across different asset classes.

Third, retail investors' tendency to chase gains and cut losses amplified liquidity pressures. The prior strong performance of gold attracted significant inflows from retail investors, who then exited en masse during the March pullback. Data indicates that net long positions of non-reportable positions in COMEX gold futures, as well as holdings of SPDR Gold ETF, dropped sharply. Retail investors' behavior of chasing gains and cutting losses further exacerbated liquidity pressures on gold.

Turkey's central bank gold sales are an isolated case, and the global trend of central banks purchasing gold remains unchanged.

The recent announcement by Turkey's central bank regarding gold sales has sparked concerns in the market about a reversal in the logic behind central banks' gold purchases. The report argues that these concerns have been overinterpreted, as Turkey's actions stem from highly specific background factors.

According to data cited by Reuters on Thursday, Turkey's central bank gold reserves plummeted by more than 118 tons over the past two weeks, with a value close to $20 billion. Last week alone, the reserves dropped sharply by 69.1 tons to 702.5 tons. This single-week sell-off set a record for the largest weekly decline since at least 2013. Additionally, estimates from three banking sources suggest that approximately 26 tons of gold were directly sold last week, while another 42 tons were utilized through swap transactions; in the prior week, gold reserves decreased by 49.3 tons.

Turkey's energy demand is highly reliant on imports, and rising oil prices have forced it to require more US dollars to purchase energy. Meanwhile, nearly half of Turkey’s official reserves consist of gold, while its holdings of US Treasury bonds are minimal, making it impossible to obtain the necessary dollars by selling US bonds. Thus, Turkey had no choice but to sell gold.

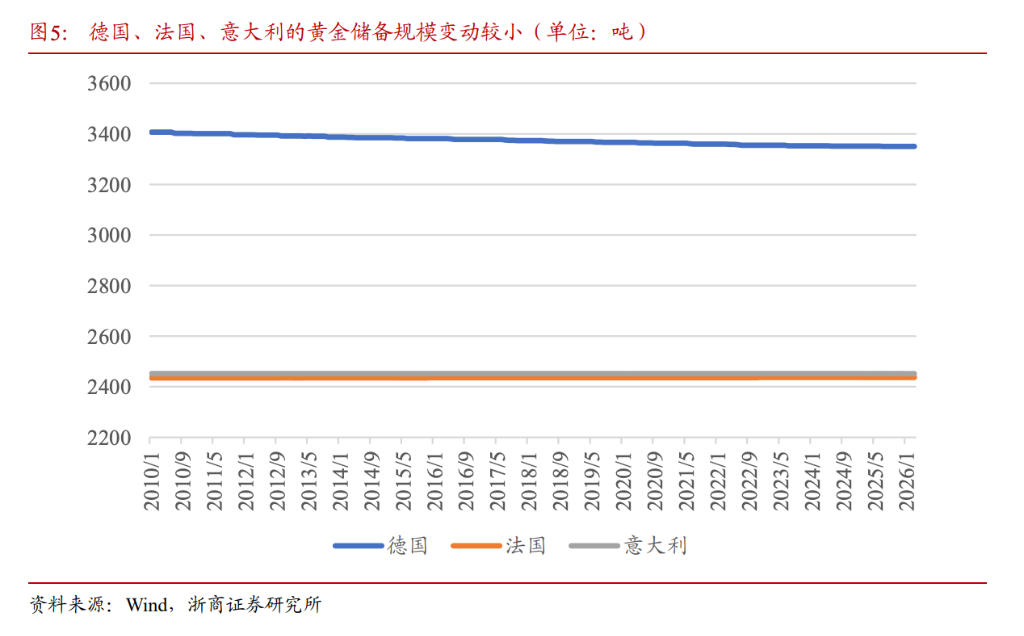

Other countries with high proportions of gold reserves and low energy self-sufficiency are mainly concentrated in Europe. Germany holds 82% of its official reserve assets in gold, France 80%, and Italy 79%. However, European countries currently still have relatively ample energy reserves, and gold plays a role in underpinning the credibility of the euro.

Data shows that the scale of gold reserves in countries like Germany, France, and Italy has remained almost unchanged in recent years. In the absence of significant liquidity pressures, the likelihood of European countries selling gold in the future is low, and the long-term trend of central banks purchasing gold will not be reversed due to Turkey's isolated case.

Market trading patterns may shift, and gold is poised to benefit from a dual-logic dynamic.

The previous market trading paradigm was: Rising oil prices equaled a pullback in rate cut expectations, meaning the market believed the Federal Reserve’s focus was on inflation. In March, the US manufacturing PMI reached 52.7, a recent high, and this trading logic flowed smoothly given the strong fundamentals.

However, if oil prices remain elevated for more than a quarter, the effects of demand destruction may begin to emerge, significantly weakening economic fundamentals. At that point, the higher the oil price, the greater the risk of recession, which could instead lead to heightened expectations for Federal Reserve rate cuts. Considering that the conflict has already lasted a month, and market expectations tend to lead fundamentals, if oil prices remain elevated, the inflection point for markets to shift from “rate hike trading” to “recession trading” may be imminent.

This creates a “dual-benefit” logic for gold:

If geopolitical tensions escalate further: markets will shift towards recession trading, expectations of interest rate cuts will strengthen, and gold will benefit;

If geopolitical tensions ease: oil prices will fall, expectations of interest rate cuts will also strengthen, and gold will similarly benefit.

In addition, following the previous decline, the issue of excessive positioning in gold may have been largely alleviated. As of March 24, the net long positions of non-commercial traders in COMEX gold (roughly representing institutions) were at the 25.3rd percentile since 2020, while the net positions of non-reportable positions (roughly representing retail investors) were at the 79.9th percentile, both significantly lower than previous levels.

The improvement in positioning structure implies that the capital-related disruptions that previously weighed on gold are nearing an end, and gold pricing is expected to gradually return to fundamental logic.

Editor/Lambor