The rebound in U.S. job growth in March, coupled with an unexpected decline in the unemployment rate, indicates that the labor market is stabilizing amid the outbreak of the Iran war.

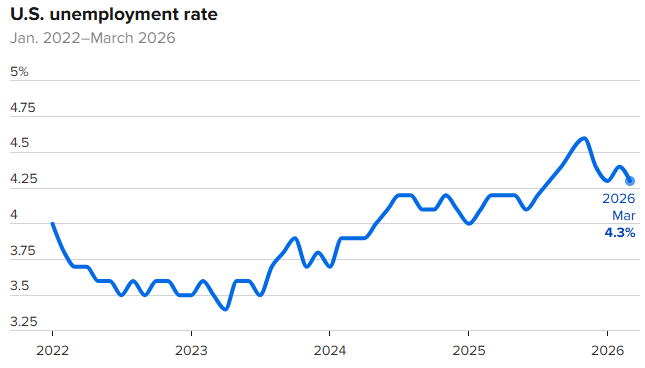

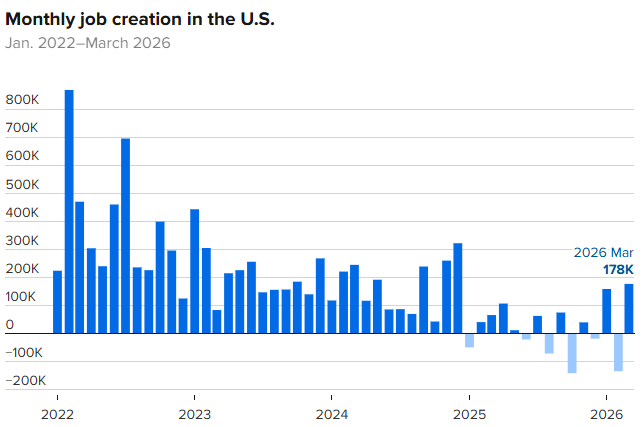

The rebound in U.S. job growth in March, coupled with an unexpected decline in the unemployment rate, indicates that the labor market is stabilizing amid the outbreak of the Iran war. The seasonally adjusted U.S. nonfarm payrolls increased by 178,000 in March, the highest rise since the end of 2024, surpassing expectations of 60,000, while the previous figure was revised from a loss of 92,000 to a loss of 133,000. The U.S. unemployment rate stood at 4.3% in March, below the expected 4.40%, with the previous figure at 4.40%.

The change in total nonfarm employment for January was revised upward by 34,000, from +126,000 to +160,000; the change for February was revised downward by 41,000, from -92,000 to -133,000. After revisions, the total employment figures for January and February were 7,000 lower than previously reported.

Analysts pointed out that employment growth is expected to accelerate until June, reflecting an increase in hiring in the leisure and hospitality sectors as the US hosts the World Cup football tournament, as well as a cyclical rebound in the freight industry. The significant supply shock caused by the outbreak of the Iran war may not be reflected in employment data until the second half of the year, when the unemployment rate is expected to rise more rapidly.

Analysts pointed out that employment growth is expected to accelerate until June, reflecting an increase in hiring in the leisure and hospitality sectors as the US hosts the World Cup football tournament, as well as a cyclical rebound in the freight industry. The significant supply shock caused by the outbreak of the Iran war may not be reflected in employment data until the second half of the year, when the unemployment rate is expected to rise more rapidly.

Although the unemployment rate declined, this partly reflects some Americans exiting the labor force — the labor force population decreased by 396,000. The US labor participation rate in March was 61.9%, the lowest level since 2021, compared to expectations of 62.1% and a previous rate of 62.00%. The labor participation rate of workers aged 25 to 54 (also known as prime-age workers) also declined. The number of people working part-time for economic reasons increased.

Economists estimate that with labor supply growth at historically low levels, fewer than 50,000 new jobs are being added each month, barely keeping pace with the growth of the working-age population. Some estimates even suggest that the breakeven point is zero or negative. Economists at JPMorgan warned that "negative growth in any given month will become more common," adding that "even if job growth is sufficient to stabilize the unemployment rate, employment figures could still be negative at least one-third of the time."

Economists generally expected a rebound in the labor market in March after a sharp decline in employment numbers in February. Previously, strikes by more than 30,000 healthcare workers and severe winter weather led to the sharp drop in employment figures in February. This strong growth could further reinforce the Federal Reserve’s focus on inflation risks, as the Middle East conflict has triggered a rapid rise in energy prices.

The growth in nonfarm payrolls in March was primarily driven by the healthcare sector, which saw a recovery following the end of strikes by employees of Permanente in California and Hawaii. The construction industry as well as the leisure and hospitality sectors also rebounded after declines in February, likely reflecting a weather-related bounce-back. The increase in nonfarm employment in the manufacturing sector hit its highest level since the end of 2023.

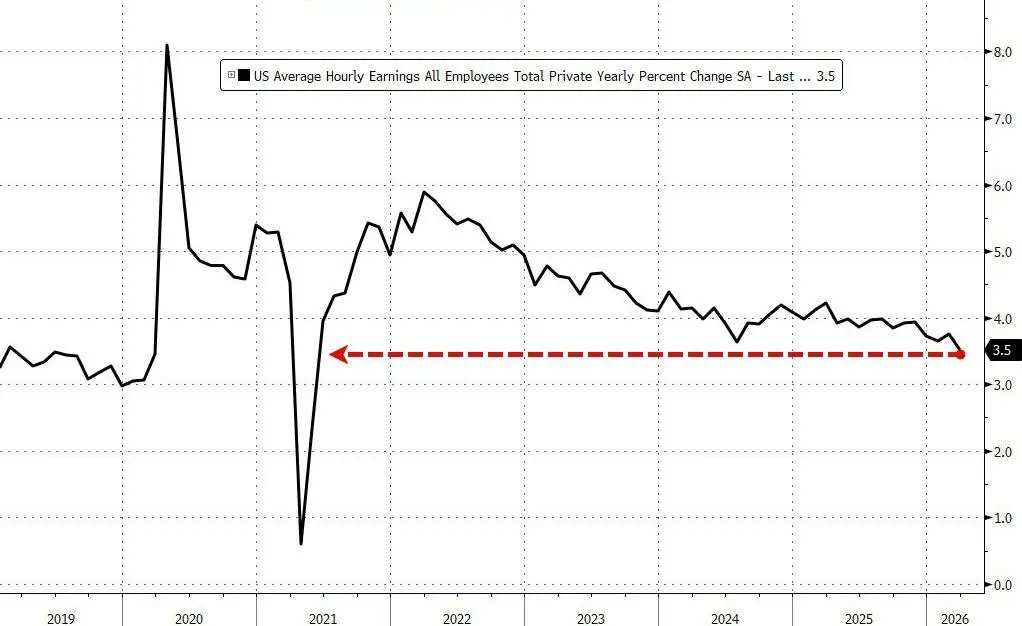

Economists are also closely monitoring how labor supply and demand dynamics impact wage growth, especially amid renewed inflation risks. The report showed average hourly earnings rose 0.2% month-on-month and 3.5% year-on-year, the lowest level in nearly five years, both below expectations.

Other data indicated that prior to the outbreak of the Iran war, there was no momentum in labor market growth. Job openings fell in February, and the hiring pace slowed to its lowest level since 2020. In March, the small business hiring plans index remained stable, staying near one of its lowest levels in recent years.

Although March may not be sufficient to reflect the impact of the Middle East conflict, some economists suggest that the April employment report could begin to show its effects. This week, the national average retail gasoline price surpassed $4 per gallon for the first time in over three years. This will push up inflation, erode household purchasing power, offset some of the strong momentum in wage growth, and suppress consumer spending. The war caused an evaporation of approximately $3.2 trillion in stock market value in March. Trump vowed on Wednesday to launch a more aggressive strike against Iran.

The March employment report is unlikely to affect interest rate prospects, as the full economic impact of supply chain disruptions caused by the conflict has yet to materialize. The likelihood of a rate cut this year has significantly diminished.

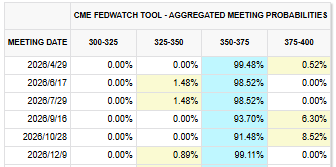

U.S. Treasury yields rose following the release of robust nonfarm payroll data, reinforcing market expectations that the Federal Reserve will maintain interest rates unchanged for a longer period rather than cutting them.$U.S. 10-Year Treasury Notes Yield (US10Y.BD)$Following the release of the employment data, the yield on the 10-year Treasury note rose by 4.7 basis points to 4.36%, while the yield on the 2-year Treasury note, which reflects rate expectations, climbed by 6.6 basis points to 3.862%. Futures markets indicate little likelihood of any action at the FOMC meeting on April 28-29, with CME FedWatch data showing a more than 90% probability that the Federal Reserve will keep interest rates unchanged through the end of the year.

Editor/Rocky