The "sell signal" of Bank of America's Bull & Bear Indicator has been lifted. Trump's approval rating continues to decline, and the political logic is pointing towards a "short war" rather than a "long war." The "4C" trade portfolio (commodities, Chinese assets, U.S. consumer stocks, and curve steepening) is favored, while cautioning about the risks of an AI bubble.

Against the backdrop of a reshaped geopolitical landscape, ongoing trade policy disruptions, and a shift in the U.S. political cycle, the "4C" trading portfolio—centered on commodities, Chinese assets, U.S. consumer stocks, and a steepening yield curve—is poised to become the most explosive investment opportunity in the second half of the year.

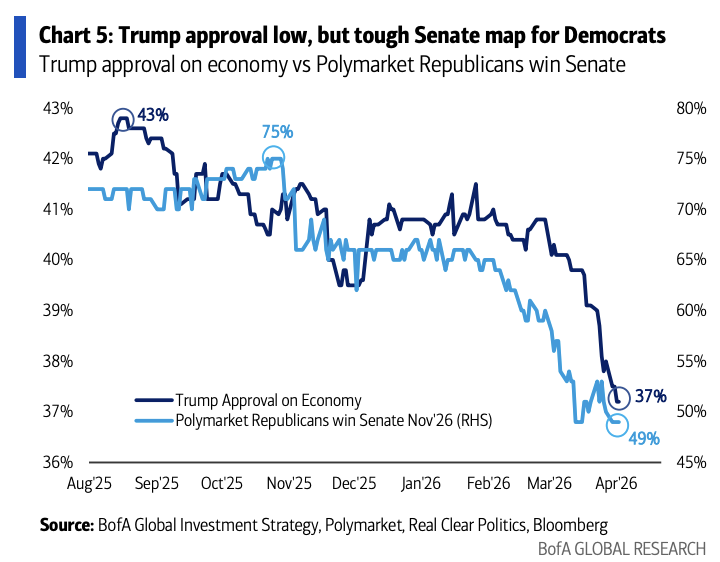

According to the ZF Trading Desk, the latest The Flow Show report issued by Bank of America Securities points out that Trump's approval ratings have continued to decline (with only 37% support for his economic policies and a mere 33% for his inflation management), leading political logic to favor a "short war" scenario over a "long war," thereby giving rise to the aforementioned four trading themes.

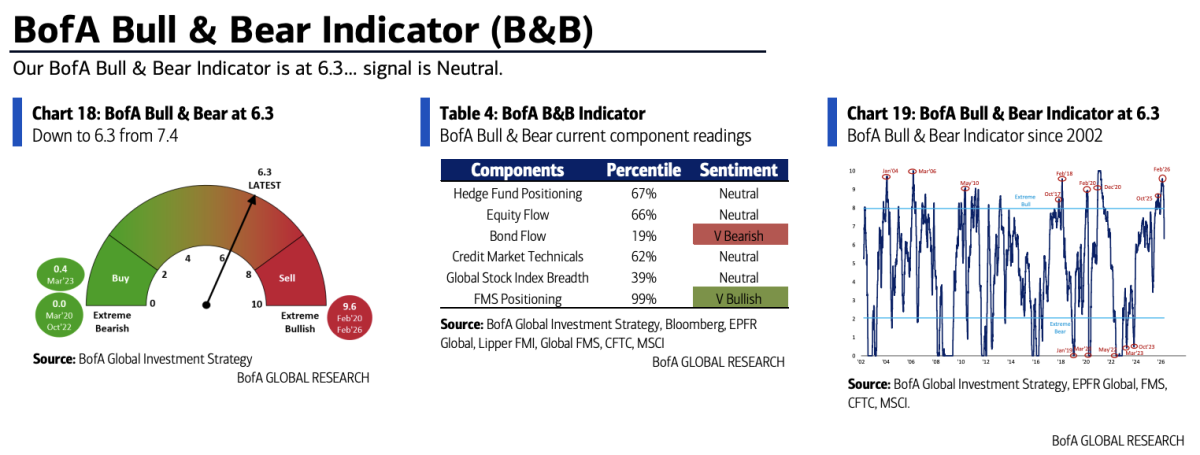

Meanwhile, Bank of America's Bull & Bear Indicator plummeted from 7.4 to 6.3, hitting its lowest level since June 2025, with the weekly drop marking the largest decline since April 2025. The "sell signal" has now been lifted. Significant net outflows from high-yield bonds and deteriorating breadth in global equity indices were the primary drags.

Meanwhile, Bank of America's Bull & Bear Indicator plummeted from 7.4 to 6.3, hitting its lowest level since June 2025, with the weekly drop marking the largest decline since April 2025. The "sell signal" has now been lifted. Significant net outflows from high-yield bonds and deteriorating breadth in global equity indices were the primary drags.

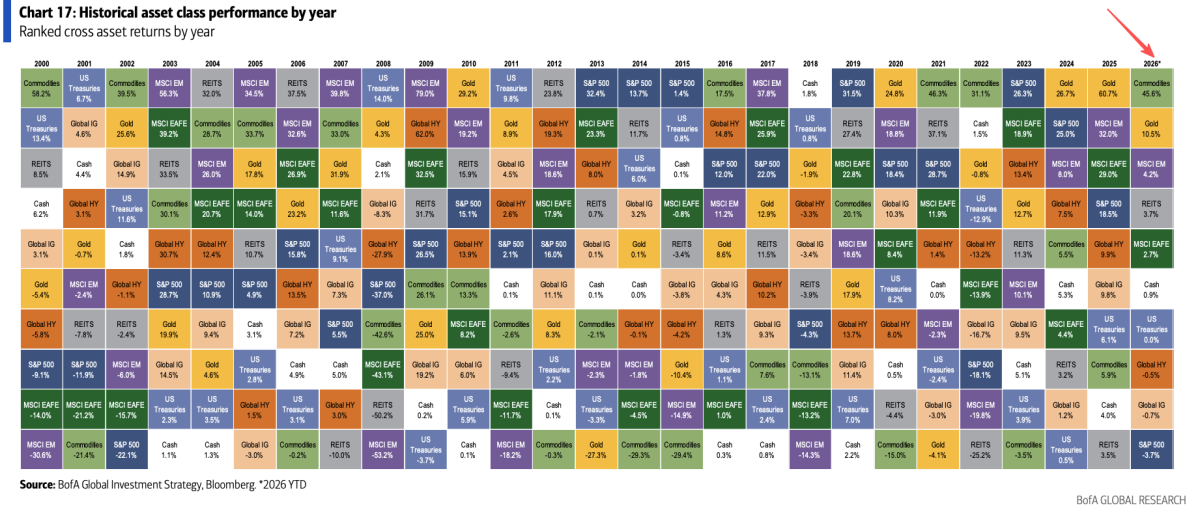

In terms of asset performance year-to-date, crude oil leads with a 74.4% surge, followed by a 45.6% increase in commodities overall and a 10.2% rise in gold. Conversely, U.S. equities fell by 3.8%, while Bitcoin plummeted by 22.2%, signaling a clear shift in market dynamics.

The sharp decline in the Bull & Bear Indicator reflects growing market caution.

Bank of America's Bull & Bear Indicator dropped to 6.3 this week, reaching its lowest point in nearly ten months, driven by three key pressures: worsening breadth in global equity indices, outflows from high-yield bonds, and widening spreads between high-yield bonds and subordinated bank debt.

The inverse "sell signal," which was triggered on December 17, 2025, was officially lifted on March 25, with the current signal now neutral.

According to Bank of America's Global Breadth Rule, currently, a net 16% of MSCI World Index constituents are trading below both their 50-day and 200-day moving averages, far from the -88% threshold required to trigger a buy signal.

Current positioning data does not indicate a full liquidation by bulls, but any rebound attempting to break above 6800 points (resistance at the 50-day and 100-day moving averages) faces significant pressure. "Selling on rallies" has now become the dominant market consensus.

"4C" Framework: Four Key Themes to Capture Opportunities in the Second Half

Bank of America's "4C" investment framework encompasses four interconnected trading directions.

Yield curve steepening: The 2-year U.S. Treasury yield failed to break through 4% effectively last week, marking the end of the flattening trend triggered by the Q1 valuation risk shock. The "ceiling" signal for the 2-year rate, combined with the weakening U.S. labor market, supports taking longer duration positions and betting on curve steepening.

Commodities: Geopolitical competition over resources provides robust support for commodities. This week, Trump announced an increase in pharmaceutical tariffs and expanded tariff coverage on steel, aluminum, and copper, further reinforcing the market’s pricing of resource scarcity.

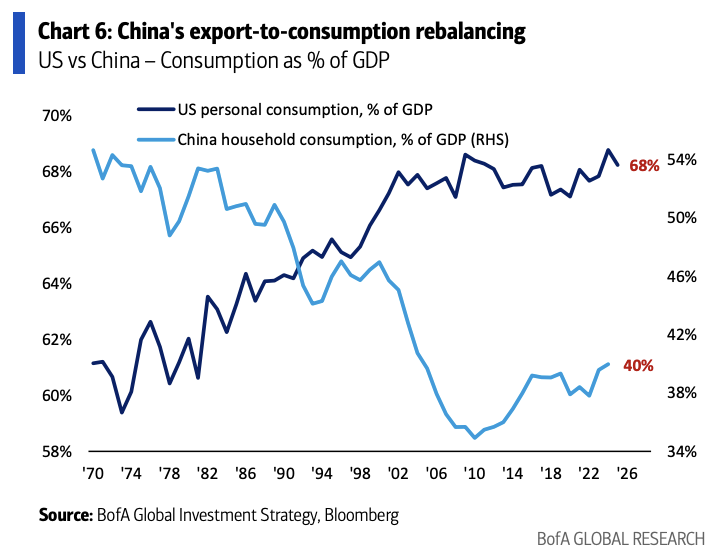

Chinese assets: The "Sino-U.S. May meeting" and the reshaping of China's consumption structure are key catalysts. Data shows that the proportion of Chinese household consumption in GDP remains significantly lower than that of the U.S., indicating substantial rebalancing potential and significant room for valuation recovery in Chinese assets.

U.S. consumer stocks: A major policy shift focusing on addressing cost-of-living issues is expected after the war ends. However, short-term capital flows show divergence: consumer sector outflows reached $11 billion this week, the largest weekly outflow since December 2025, suggesting the allocation window for consumer stocks may not yet be open.

Soft landing or hard landing? Liquidity-sensitive assets are the indicators.

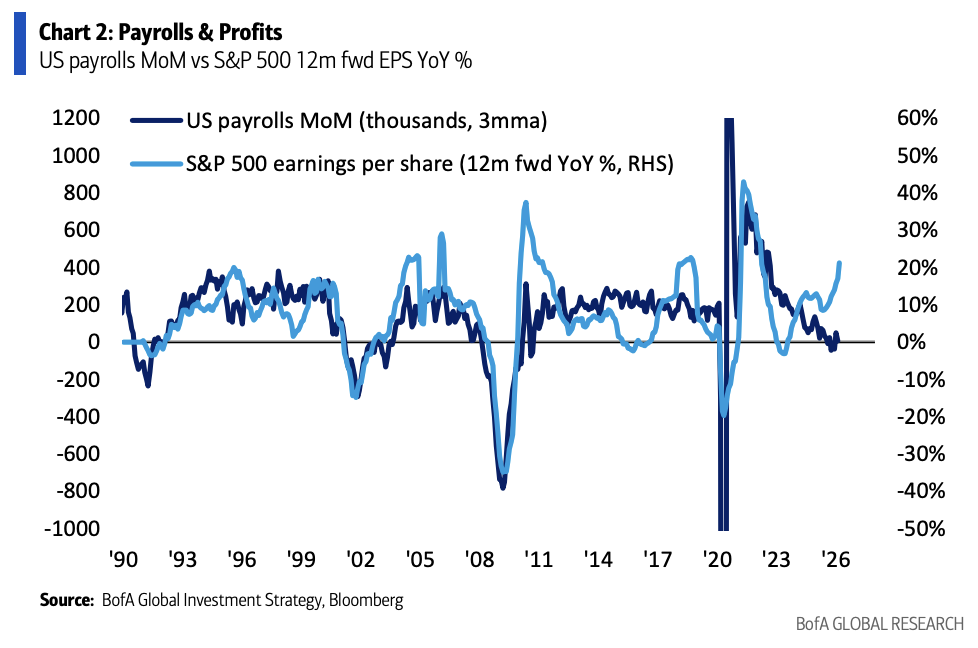

The core contradiction in the current market focuses on the interaction between employment and corporate earnings.

Nonfarm payroll data correlates positively with the S&P 500’s 12-month forward earnings per share (EPS). With the 2026 EPS forecast for the S&P 500 having been revised upward from $310 at the beginning of the year to $323, continued strong employment data in the coming months could prevent earnings expectations from following stock prices downward.

The tipping point for determining a soft or hard landing is also clear: If liquidity-peak impaired assets such as Bitcoin, private credit, software ETFs, and bank stocks can stabilize and rebound against a backdrop of peaking yields and curve steepening, the probability of a soft landing will be higher; if these assets fail to find bottom support, the risk of a hard landing will rise significantly.

From a political perspective, Trump’s declining approval ratings are repricing the midterm election landscape— the probability of Republicans retaining the House has dropped to 15%, while the likelihood of holding the Senate has fallen back to 49%. The core policy risk in Q2 lies in trade policy once again becoming a tool for the U.S. to exert geopolitical pressure.

Bank of America maintains its short position on AI data center bonds, with private client equity allocations dropping to near one-year lows.

Data from Bank of America's Global Wealth and Investment Management (GWIM) division shows that private clients manage assets totaling $4.1 trillion, with equity allocations falling to 63%, the lowest since May 2025. Bond and cash allocations rose to 18.6% and 11.0%, respectively, both recording net inflows this week.

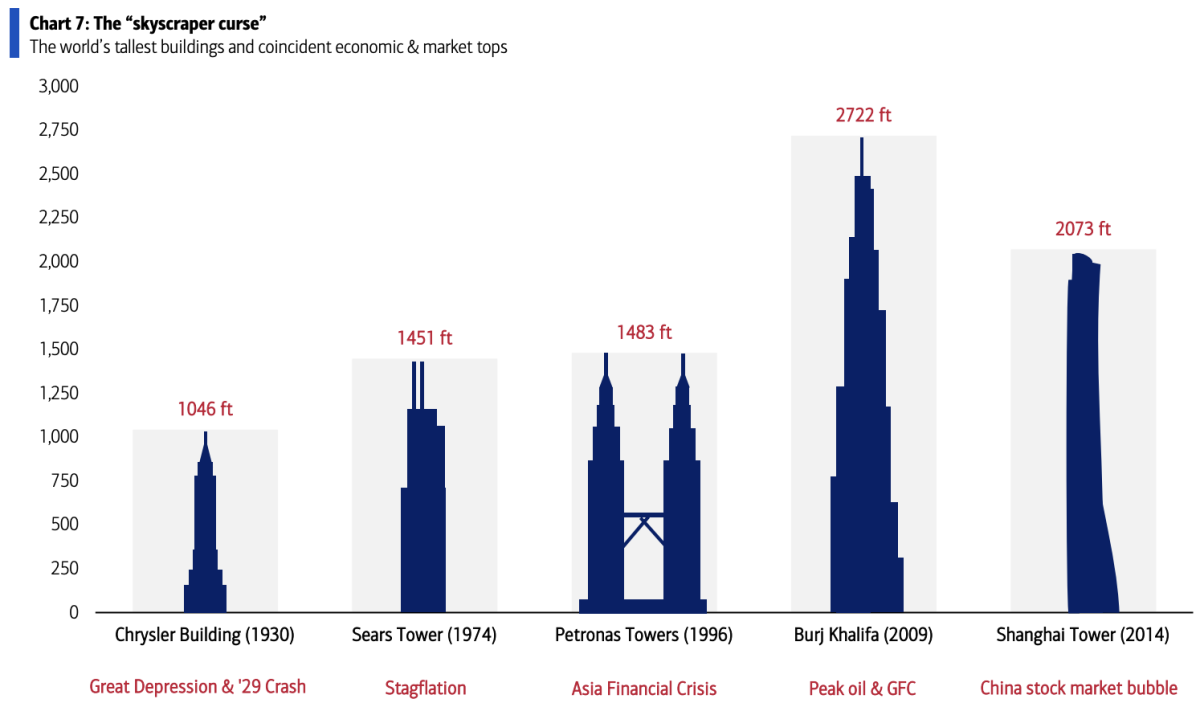

The "Skyscraper Curse" — historically, the completion of the world’s tallest buildings has often coincided with the peak of economic bubbles. Bank of America argues that the hallmark of this cycle will not be the tallest building but the largest AI data center — the Delta Gigasite project in Utah, which is expected to provide over 10 gigawatts of computing power, with construction starting at the end of 2025 and initial power supply anticipated by 2027.

Based on this assessment, Bank of America maintains its stance on shorting corporate bonds of AI hyperscale data center operators and notes that Microsoft, Meta, and Oracle have recently undertaken significant layoffs to fund data center capital expenditures, viewing this as a signal of worsening capital misallocation.

Editor/Jayden