Authors: Wu Shuo, Lin Yan

Source: Chuan Yue Global Macro

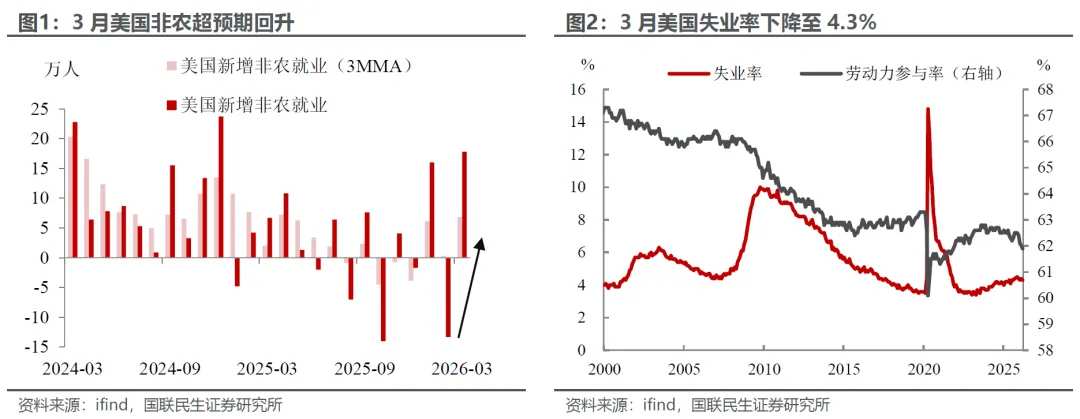

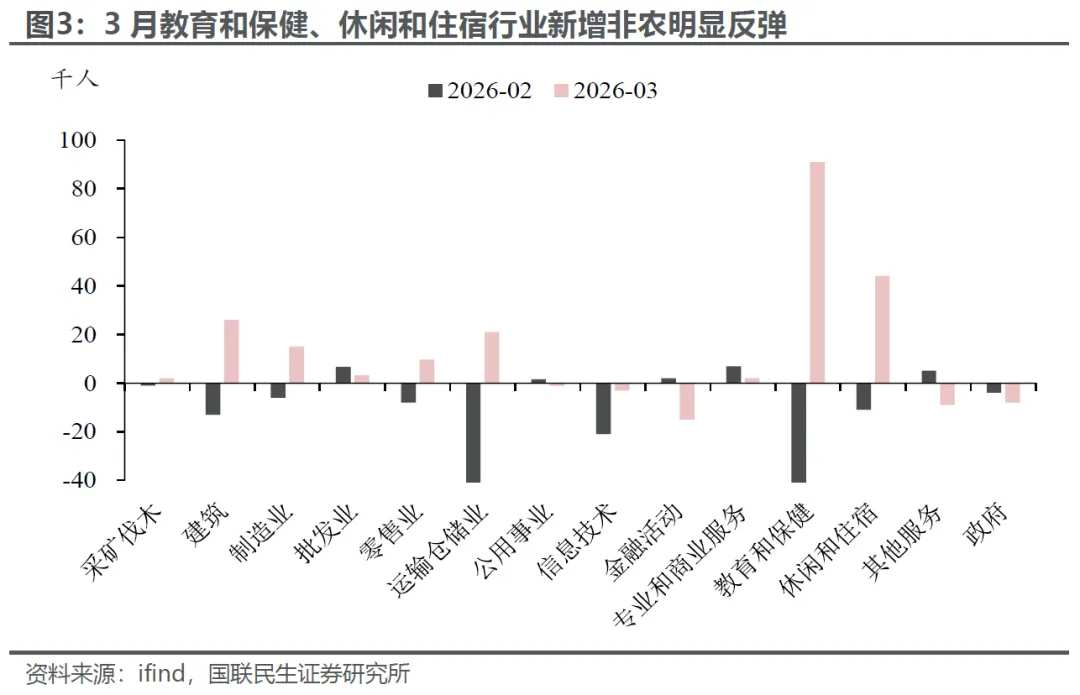

The strong rebound in March's nonfarm payroll data erased the weakness seen in February and caught the market off guard. Not only did the economy add 178,000 new nonfarm jobs, significantly surpassing market expectations, but the unemployment rate also fell to 4.3%, signaling a dual boost for economic data. However, against the backdrop of high oil prices, the recovery in the job market in March undoubtedly added more complexity to this year’s monetary policy outlook. Following the release of the data, the market reacted swiftly, with the dollar index climbing back above the 100 mark and U.S. Treasury yields experiencing a short-term spike.

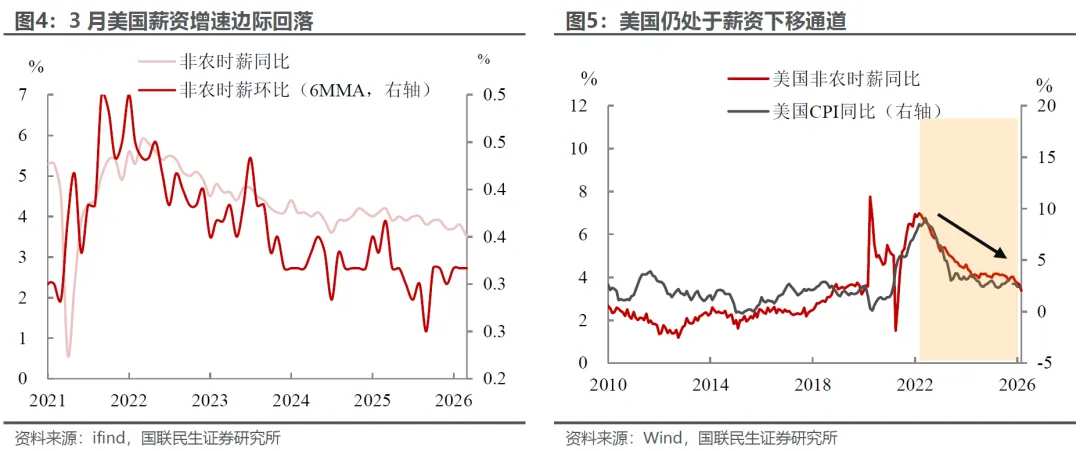

How should we interpret the strong rebound in March's nonfarm payroll? The main factors were the resolution of strikes and extreme weather conditions seen in February. On one hand, the end of strikes directly drove a significant recovery in education and healthcare employment, adding 91,000 jobs, which became the core driver of March’s new nonfarm payrolls. On the other hand, the dissipation of winter's extreme weather effects allowed employment in offline service sectors such as construction (26,000 people) and leisure and hospitality (44,000 people) to recover somewhat, essentially reflecting a concentrated rebound in previously suppressed demand.

However, upon closer inspection, the nonfarm payroll figures are not as robust as they appear on the surface. After smoothing out the new nonfarm payroll additions from January to March, the average monthly increase was about 70,000 people—though higher than the second half of last year, overall employment momentum remains weak. Additionally, while the unemployment rate fell to 4.3%, it was partly supported by a decline in labor force participation, rather than being entirely due to substantial improvements in employment demand.

However, upon closer inspection, the nonfarm payroll figures are not as robust as they appear on the surface. After smoothing out the new nonfarm payroll additions from January to March, the average monthly increase was about 70,000 people—though higher than the second half of last year, overall employment momentum remains weak. Additionally, while the unemployment rate fell to 4.3%, it was partly supported by a decline in labor force participation, rather than being entirely due to substantial improvements in employment demand.

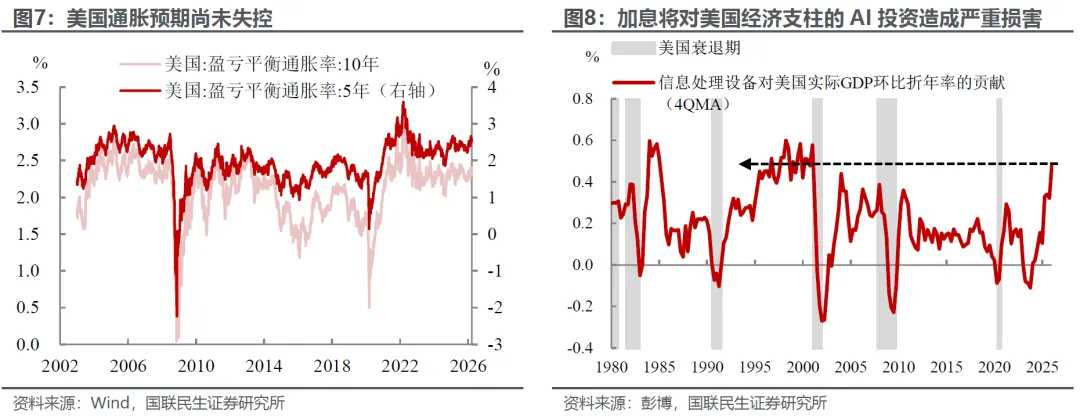

More importantly, wage growth showed a clear slowdown. In March, both the year-on-year and month-on-month growth rates of hourly wages dropped to 3.5% and 0.2%, respectively. This alleviated the Federal Reserve’s concerns over a wage-inflation spiral and also helped weaken the transmission of upstream costs to downstream inflation.

Moreover, the March nonfarm payroll data has not fully accounted for the impact of escalating conflicts in the Middle East. The potential impacts on economic growth and micro-level expectations remain to be seen and may exhibit lagging effects. Coupled with the non-manufacturing PMI falling below the breakeven line, the momentum in the services sector has further weakened. It is still too early to conclude that the job market has entered a trend reversal toward sustained recovery.

In terms of monetary policy, the impact of this unexpected nonfarm payroll report is actually limited. In fact, before the release of March’s nonfarm data, market expectations for the Fed’s interest rate cuts this year had already been largely priced in, with the timing of rate cuts even pushed back to the second half of 2027. Thus, the marginal impact of this employment data on expectations was relatively small.

In the short term, inflation remains a much higher priority than employment in the Fed’s policy considerations. Once there are signs of easing tensions in the Middle East and upward pressure on oil prices subsides, inflation expectations are likely to fall significantly. At that point, the constraints on the Fed’s policy will ease noticeably, creating more room for interest rate cuts.

As for expectations of an interest rate hike by the Fed this year, we still believe the threshold is too high. In our report 'Will the Fed Restart Rate Hikes This Year?', we noted that with the job market yet to stabilize and downstream demand remaining weak, the Fed does not currently have the conditions necessary to raise rates. Moreover, in an election year, the economic damage caused by rate hikes would be difficult for the Trump administration to bear.

For the asset side, the market remains in a 'crossing the river by feeling the stones' state. Although we have consistently emphasized the medium- to long-term rationale for resources such as gold, short-term statements by Trump have been highly volatile, with policy expectations continuing to swing, and asset volatility has yet to stabilize. Despite the fact that the current U.S. bond market, gold, and equity markets have already priced in significant pessimistic expectations and geopolitical risk premiums, against the backdrop of unresolved tensions and unclear policy direction, it remains difficult to establish a trend-based market. In this environment, reducing overall positions and contracting risk exposure may be a more prudent choice.

Looking ahead to the second quarter, we believe that in the context of continued upward price pressures, the core of short-term asset allocation lies in capturing inflation pass-through chains with effective end-price transmission capabilities. Currently, the inventory cycles of major global economies are in a downward or bottoming-out phase, and terminal demand with genuine purchasing power is concentrated in two primary areas: first, the rigid demand brought about by the global artificial intelligence industry cycle; and second, sovereign reserve restocking driven by geopolitical security logic. Related sectors are expected to foster phased investment opportunities. We will provide a detailed elaboration of the above logic in subsequent reports.

Risk warnings: Unexpected stickiness in U.S. inflation and tariff pass-through; escalation of geopolitical conflicts and significant increases in oil prices; unexpected shifts in U.S. fiscal policy; potential discrepancies in data calculations.

Editor/Melody